US home prices up 9.3 pct., most in nearly 7 years

Source: AP-Excite

By CHRISTOPHER S. RUGABER

WASHINGTON (AP) - U.S. home prices rose 9.3 percent in February compared with a year ago, the most in nearly seven years. The gains were driven by a growing number of buyers who bid on a limited supply of homes.

The Standard & Poor's/Case-Shiller 20-city home price index increased from an 8.1 percent year-over-year gain in January. And annual prices rose in February in all 20 cities for the second month in a row.

Phoenix led all cities with an annual gain of 23 percent in February. Prices jumped nearly 19 percent in San Francisco. In Las Vegas, home prices increased 17.6 percent and in Atlanta they rose 16.5 percent.

Eleven of the 20 cities reported price gains in February compared with January. Those monthly numbers are not seasonally adjusted and reflect the slower winter buying period.

FULL story at link.

Read more: http://apnews.excite.com/article/20130430/DA5VT89O1.html

In this Tuesday, March 5, 2013, photo, a home is for sale in Auburn, N.H. Standard & Poor's/Case-Shiller reports on home prices in February on Tuesday, April 30, 2013. (AP Photo/Charles Krupa)

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

SleeplessinSoCal

(9,112 posts)I don't know how widespread this is, but it's a really bad sign for the future.

jakeXT

(10,575 posts)“It’s happening in the most speculative sub-prime markets, where massive amounts of 'fast money' is rolling in to buy, to rent, on a speculative basis for a quick trade,” he contends. “And as soon as they conclude prices have moved enough, they’ll be gone as fast as they came.”

By 'fast money', Stockman is referring to professional investors like hedge funds and private equity firms. To his point, global investment firm Blackstone (BX) has spent more that $2.5 billion on 16,000 homes to manage as rentals, according to Bloomberg. It’s now the country’s largest investor in single-family homes to manage as rentals, with properties in nine markets. And Blackstone is joined by others like Colony Capital LLC and Two Harbors Investment Corp. (SBY) in trying to turn this market into a new institutional asset class, Bloomberg reports.

http://finance.yahoo.com/blogs/daily-ticker/housing-bubble-2-0-david-stockman-133026817.html

Yo_Mama

(8,303 posts)I was struggling to prevent client banks from adopting the "special mortgages" and warning of widespread disaster. Lost clients and took ALL sorts of abuse for it. I just got kicked around the block for fighting the tide, and for a while the bank supervisory agencies were no help either.

The thing that killed me then is that a lot of average people realized the problem when experts didn't. By "experts" I mean the top-line experts, including many Fed economists. At the time I concluded that there are limits to expertise because in fact experts often have less knowledge than average individuals.

And you, my friend with the good eyes and active mind, are the NEXT example of why representational democracy really does work - because you're absolutely right. Over the last year, the number of houses occupied by homeowners has continued to drop because the got-cheap-money-investors are buying up these houses to rent. For short-term appreciation. All the increase in occupied homes has been in rentals.

Worse yet, with the barrier for actual first-time buyers rising due to FHA premium and term increases, the relative split between the cost charged to private equity versus would-be owner-occupiers keeps rising.

This is a recipe for disaster. Actual owner-occupiers insert great stability into the housing market, but investors create instability.

It's already gotten so bad that houses are being sold in bulk from the original investors to the next tier of got-rocks big boys. That's a sign of big trouble to come. Add to that falling rents in some areas with heavy investor activity, and the warning signals are blinking. Once again, the experts are pushing a trend that cannot end well. And once again, this includes Fed economists.

What's missing from this "recovery" are the first-time buyers, and until they come back, the market will not be stable. Now this isn't true in all areas, but there are impending problems in many areas.

SleeplessinSoCal

(9,112 posts)From last September:

SACRAMENTO -- Attorney General Kamala D. Harris today announced that the final parts of the California Homeowner Bill of Rights have been signed into law by Governor Jerry Brown.

http://oag.ca.gov/news/press-releases/attorney-general-kamala-d-harris-announces-final-components-california-homeown-0

That would be addressing past problems. What about those you wrote about so terrifyingly re: the lack of new home ownership? Could it be some are too fearful of the system and choose to rent?

Yo_Mama

(8,303 posts)Home prices rose way too fast in the bubble (as we all know) for most to save even a minimal downpayment. It's quite easy to save 5K for a 100K house. It's a lot harder to save 20K for a 400K house.

Also student loans are weighing on a lot of the younger crew that did get decent jobs. It's not that they are not saving, but their savings are going to pay down those student loans which have relatively high interest, and who the heck wants to buy a house when you have $100K in student loans at 6%?

There is no possible banking regulation solution, because a good chunk of the 85 billion a month the Fed is dumping into the economy is going into housing.

Last time the Fed QE'd, it ran commodities and so forth up. But no one believes in $200 a barrel oil any more. We know how that's going to end. And stock valuations have been way run up. So now the private equity types and the Black Rocks are quite literally buying houses. The problem is that when you read that Atlanta area houses increased 16% in a year, you also know darned well that the incomes of the potential first-time buyers didn't. The best they could have done would have been 2%.

What happens when interest rates go back up? They will when the Fed finally backs off!

If younger people want to buy a first home, they'll save for it. 3.5% shouldn't be that big a deal. But when prices are rising FASTER than they were for much of the bubble, you have to believe that they are getting priced out of the market!!! And the pressure on now is to lower mortgage standards again, so that we go back to no-downpayment loans. Well, that isn't the solution.

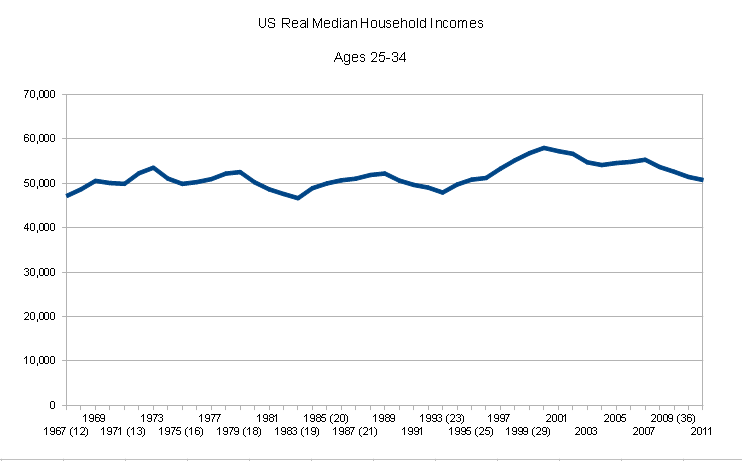

Because household incomes didn't rise that fast. Real disposable incomes for households were still falling as of 2011. Especially in the 25-34 age bracket.

SleeplessinSoCal

(9,112 posts)Right now I've got HGTV on airing a new series on house flipping. Those were common on various stations before the crash. This is the first night I've seen one on the air since 2008. The people showcased in it now look like vultures to me.

Thanks for all the info. I still don't understand how banks get away with charges for a 30 year home loan. Makes renting seem sane and fiscally responsible, were it not for those who actually wind up with someone's hard earned pay.

Yo_Mama

(8,303 posts)It's running a hefty loss due to prior lending, so it is raising its fees to try and stay solvent. FHA insures loans - it does not make them.

FHA exists solely to help individuals qualify for mortgages who otherwise would not be able to get them.

SleeplessinSoCal

(9,112 posts)"Poor people did it". Was the answer I heard regularly from the right when the Bubble burst. It was made clear by various books and investigative reporting that it was in fact the fault of those making the loans and the lack of transparency, while selling junk loans and betting against itself. Yet these are the people in charge of who gets or doesn't get to buy a home. It's twisted.

It's the Banks that have all the money while refusing to risk even a decent loan to a decent buyer and stymieing economic growth that goes with the housing market. Similarly, my auto insurance company put me in a "high risk" category for having a fender bender. No tickets, no other accidents, a perfect record, yet they raised my rates because they want no risk and make more money than they've earned. I left them because I had an option. It's not possible when trying to take advantage of a buyer's market when only banks and investors can buy property.

Also, when we purchased our home 15 years ago we were fortunate in that it wasn't easy to get a loan. But we qualified. We've never been under water. We would not qualify for a loan if we had entered the market today. And I suspect many, many potential buyers are in the same place we were 15 years ago.

reformist2

(9,841 posts)The spike up happened late last year when interest rates dropped again.

yellowcanine

(35,699 posts)May not be a good thing. Buyers with limited cash for down payments and mediocre credit could be pushed out of the market very quickly.

SleeplessinSoCal

(9,112 posts)However, if some family home buyers have been waiting for the market to bottom out before making an offer, this may trigger a wider rally. It's the fact that the banks aren't lending as they would normally that's also troubling.

Where does Jack Lew stand on all this?

"“A great deal of work remains to attract private capital to our nation’s housing finance system and bolster a housing market showing signs of recovery,” Lew said. “We need to strengthen markets that may be susceptible to destabilizing runs and fire sales. We need to increase our vigilance to operational risks, whether from cyberattacks or from devastating acts of nature like we saw with Superstorm Sandy. And we must work with our foreign counterparts to reform the governance and integrity of financial benchmark reference rates like Libor and to consider transitions toward alternative benchmarks.”

http://bankcreditnews.com/news/treasury-secretary-lew-financial-system-stronger-but-much-work-remains/9820/

Hurricane Sandy hadn't entered my mind.

Yo_Mama

(8,303 posts)Investor buying is crowding out first-time purchasers.

You know those chuckleheads will be selling later.

byeya

(2,842 posts)the past 8 years or so reports Friday: New Home sales up 1.5% on the back of a 6.8% decline in prices; mortgage applications for home purchases(which is good at screening out investment buying) is just above the housing crisis level; The National Ass'n of Home Builders index of sentiment has declined for the 3rd month in a row - and this is the most upbeat season for this sector - and real final sales, which strips out inventory changes - showed a continued deceleration to 1.5% down from 2.4% in 2012's 3rd quarter.

I think the building stocks have gotten ahead of reality.