General Discussion

Related: Editorials & Other Articles, Issue Forums, Alliance Forums, Region ForumsObamacare Winners & Losers (in Pie Chart form)

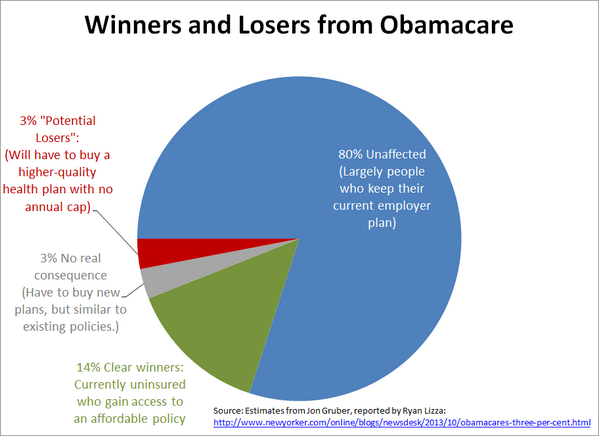

Gruber, called the architect of Romney's successful health care plan in Massachusetts, argues that of the six percent of Americans who buy their own health care on the individual market, three percent would have negligible change to their policies. He also addresses President Obama's memorable but over-simplified promise, that if you like your plan, you would be able to keep it. From Lizza's writeup:

“We’ve decided as a society that we don’t want people to have insurance plans that expose them to more than six thousand dollars in out-of-pocket expenses,” Gruber said. Obama obviously should have known that his blanket statement about “keeping what you have” could not apply to this class of policyholders.

Gruber summarized his stats: ninety-seven per cent of Americans are either left alone or are clear winners, while three per cent are arguably losers. “We have to as a society be able to accept that,” he said. “Don’t get me wrong, that’s a shame, but no law in the history of America makes everyone better off.”

TPM

Now Fox News needs to track down those 3% and get 'em on tv.

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

winter is coming

(11,785 posts)Humanist_Activist

(7,670 posts)exchange plan without subsidies, and don't quite fall in the 9.5% threshold to opt out.

Puzzledtraveller

(5,937 posts)but I cannot afford to use it, it is a pretty good plan and my monthly contribution is small for a single person yet still I cannot afford to use it. As it is employer provided I am not eligible for subsidies at all, help with copays or deductibles, even if someone with the same income yet does not have employer provided health insurance is.

Humanist_Activist

(7,670 posts)since I'm hourly it varies, and gross I bring home about 1600 to 1900 dollars a month. The plan in question doesn't pay for ANYTHING until I pay the 2000 dollar deductible, which, at my salary, is pretty much an additional 10 percent of my income, so I have the joy of, if I wanted to use the health coverage work provides, paying 1/5 of my income, approximately, on health care. That's real affordable.

ON EDIT: Note that 1/5th of my income, approximately 4,000 dollars or so, is bear minimum, and half of it doesn't contribute to out of pocket maximums, I'm referring to the premiums, also, if I took prescription drugs, the copays on those, at 10 dollars a generic/35 dollars name brand, doesn't contribute to either deductible or maximum out of pocket, so if I need a lot of medications, that's more of my income going to medical care on top of deductible/max out of pocket/premiums.

JDPriestly

(57,936 posts)the ACA. It wouldn't take much to change the law and cover you.

eqfan592

(5,963 posts)winter is coming

(11,785 posts)and I think the percentage would be higher.

eqfan592

(5,963 posts)That being said, I'd like to find clarification, tho I don't think the percentage would much higher, as even three percent represents a lot of people.

Lifelong Dem

(344 posts)they won't be given any penalty for not taking an insurance plan according to Jay Carney.

Starting at the :37 second mark.

winter is coming

(11,785 posts)as if they've become a healthcare "winner" by not having to pay a penalty? They're not even deserving of a wedge saying, "unaffected but still uninsured"?

Lifelong Dem

(344 posts)They probably fit into a category of fucked by a Republican.

winter is coming

(11,785 posts)

ReverendDeuce

(1,643 posts)I know my plan inside and out. I'm not going to re-litigate this in this thread. Suffice to say, I've tried to explain how my perfectly decent plan being cancelled only to be bludgeoned with insults and attacks my fellow Democrats here on the forum as if defending the ACA was a religion.

My plan was just fine and the ACA is making my insurance company take it away, charge me more, and leave me with a higher deductible, 4 x higher max out-of-pocket, etc.

Not only that, but I get a 60% premium hike for the privilege.

Not pleased.

Capt. Obvious

(9,002 posts)If you're looking for a sympathetic ear there's radio and tv shows looking to book you.

ProdigalJunkMail

(12,017 posts)bollocks..

sP

KG

(28,752 posts)Cali_Democrat

(30,439 posts)Funny that!

winter is coming

(11,785 posts)Your insurance company may be trying to up-sell you into a more expensive plan than would be available on the exchange. Wendell Potter was talking about this the other night on MSNBC. Apparently, it's been a common practice of insurers for years to cancel policies and offer far more expensive/less generous ones without telling their customers that other options are available.

Capt. Obvious

(9,002 posts)in the countless threads he's banged his cup in.

ProSense

(116,464 posts)If it's a high quality, grandfathered plan, same question?

JDPriestly

(57,936 posts)and using this opportunity to charge more. The insurance companies could simply bring the plans into compliance with the ACA and charge the same rates. If they cannot do that financially then it is a sign that the plan was not as good as some of the people insured by it think it was.

The insurance companies still can decide what they offer and how much they charge for it. If the plans were all that great to begin with, the insurance companies would teak them slightly, bring them into compliance with the ACA and charge the same amount they charged before the ACA>

The fact that people are claiming that their plans are being cancelled is what makes me think that those insured by the plans did not realize how bad they were.

There may have been a lot of fine print about not covering pre-existing conditions or procedures and treatments not included in the plan. Many although not all of those limitations are out now.

The very people complaining the most have the most to gain from the ACA.

questionseverything

(9,657 posts)from the exchange would be 26% of our income

we already pay 20 %plus in taxes

roof over head around 25%

/////////////////

these plans all run around 25-30% if you actually have to use them...that just is not doable for most peops

JDPriestly

(57,936 posts)Otherwise, we should require your employer to pay for your insurance.

Are you eligible for a subsidy? Have you checked on that?

questionseverything

(9,657 posts)honestly to just have survived the housing crash in 08 i feel pretty lucky

at 55 i can not work the hours i could 20 years ago so making a ton more money would be tough and the competition for jobs is tougher than ever with all the manufacturing jobs gone

the 26% is with a subsidy

when i worked for obamas campaign (as a private citizen) i knew i would have to pay into something if we got national healthcare plans but i never dreamed the costs would be such a high percentage of income

JDPriestly

(57,936 posts)It is a real advantage to be able to go to the doctor.

questionseverything

(9,657 posts)since then we have been self pay which has been ok until now but of course we want the security insurance gives too

luckily these things can be worked out,once the problem is defined

thank you for your courteous answer and empathy

Doctor_J

(36,392 posts)They're as predictable as Fox nation.

eqfan592

(5,963 posts)The ACA had a grandfather clause for existing plans that didn't meet the minimum requirements.

DevonRex

(22,541 posts)I'd like to know. Is there another thread where you explained it that you could link me to?

subterranean

(3,427 posts)His previous plan didn't cover some things that are required under the ACA, like maternity, mental illness and substance abuse treatment, and pediatric dental and vision, which he didn't need. Deductibles, coinsurance and annual out-of-pocket costs were all better than the new bronze plan he was offered.

DevonRex

(22,541 posts)There's an asterisk at the top of the page on his BCBS right after it says - your new plan*.

I sure would like to see what that asterisk relates to, wouldn't you? Something like, of course we have other policies you can choose from as well... Or shop the ACA site or call your insurance agent, etc...

Who knows?

geek tragedy

(68,868 posts)http://thinkprogress.org/health/2013/10/31/2868631/essential-guide-debunking-obamacare-cost-myth/

1. What does the old plan actually cover? Most of the policies in the existing individual health care market — which are currently issuing notices — offer low premiums, but also come with skimpy benefits and high out-of-pocket costs. These plans often have low limits for outpatient treatment, hospitalization or don’t offer any benefits for procedures like colonoscopy, chemotherapy or mental health treatment. Insurers market these policies to young and healthy people who don’t use their coverage — and never know the true extent of their benefits. (The market is also fairly mobile, with just 17 percent of individual subscribers purchasing the same plan for two years or longer.)

Under the Affordable Care Act, insurers cover 10 essential categories of benefits, offering far more comprehensive coverage than what’s available in most individual insurance plans.

2. Did this person go to the exchanges? Insurers informing policy holders that their health care costs will go up, often direct beneficiaries to their other brand products without telling them about competitive options and prices available through the exchanges. Cavallaro, for instance, got a quote from a broker, but did not explore the available options on her own.

Prices are lowest in areas with the most insurer competition. An analysis from the McKinsey Center for U.S. Health System Reform found that “new entrants into the market make up 26 percent of all insurers,” and “tend to price their plans lower than the median premiums in their market.” The average premium in the exchanges is 16 percent lower than previously projected.

3. Yes, the premium is low, but what are the co-pays and deductibles? This coverage often forces individuals who do use care to meet high deductibles — the amount you pay out-of-pocket before your insurance kicks in — pay high co-pays and co-insurance or limit the number of doctor visits that are allowed. Cavallaro, for instance, must meet a deductible of $5,000 a year and has an out-of-pocket cap of $8,500 a year. The plan covers just two doctors’ visits and each include a $40 co-pay.

As the LA Times’ Michael Hiltzik points out in California, Cavallaro could sign-up for a Silver level plan with a $2,000 deductible, maximum out-of-pocket cost of $6,350, pay $45 for a primary care visit and $65 for a specialty visit — “but all visits would be covered, not just two.”

The health law sets exchange enrollees’ maximum annual out-of-pocket costs at $6,350, and silver plans have deductibles ranging from $1,500 to $5,000.

4. Does this person qualify for subsidies? Americans between 100 and 400 percent of the federal poverty line ($46,000 for an individual, or about $78,000 for a family of three) qualify for tax credits under the law. Six of the 7 million individuals who are expected to sign up for insurance through the exchange will receive an average tax credit of $5,290 per year.

ReverendDeuce

(1,643 posts)1. Everything the ACA covers, other than mental health, pediatric dental/vision, and maternity.

2. Yes, I did. Said it exhaustively over and over and over but nobody seemed to listen. They were too busy calling me a troll. All of the ACA plans in my area are around the same price. None are less than $200/mo.

3. I already answered this as well. $1,500 deductible, $1,500 max out of pocket, 0% copay is what I had. Thanks to ACA, the plan they want to shift me into is $2,500 deductible with a $6,350 max out of pocket and a 50% copay.

4. No. I do not qualify for subsidies.

DevonRex

(22,541 posts)And you didn't post what the asterisk went to...

http://www.democraticunderground.com/?com=view_post&forum=1002&pid=3824490

Response to Capt. Obvious (Original post)

lostincalifornia This message was self-deleted by its author.

AnneD

(15,774 posts)ITA and said as much at the time. And no one has explained how ACA this is easier than universal coverage. Looking at all the money poured in so far...universal care keeps looking better and better.

edited to add...I still think ACA was Obama's big sloppy wet kiss to the Insurance companies IMHO

Response to AnneD (Reply #14)

lostincalifornia This message was self-deleted by its author.

Doctor_J

(36,392 posts)He gave away the po before the discussion even started. He did it to keep big insurance money flowing. It is a disgrace.

Response to Doctor_J (Reply #19)

lostincalifornia This message was self-deleted by its author.

solarhydrocan

(551 posts)The biggest- UnitedHealth group inc. 5 yr chart:

See to believe:

Link for multiple charts on AET AFL AIZ CI CNC CFIN HNT HUM SIE TMK UNM WLP

http://finance.yahoo.com/quotes/AET+AFL+AIZ+CI+CNC+CFIN+HNT+HUM+TMK+UNM+WLP/view/dv

gussmith

(280 posts)when I see that 3% will have to pay more for a plan when they were part of the system before the ACA. Let's turn that Farm subsidy for the corporate farm owners into a payment to make the 3% whole.

ProSense

(116,464 posts)http://www.democraticunderground.com/10023956700

flamingdem

(39,319 posts)In fact the states without Medicaid expansion allows those making very little to get access to the PPO and other plans for under 50-100 a month with subsidies. That's way BETTER than the average Medicaid program where one can wait for months for a doctor..

CountAllVotes

(20,877 posts)I'm fortunate and I realize it and I am grateful for it and yes, I thank my Union for it. Although I am retired, I still voluntarily pay union dues.

Here's a  for my Union!

for my Union!

They were very smart and signed a 5-year contract with the carrier about 6 mos. ago. *whew*

bvar22

(39,909 posts)

woo me with science

(32,139 posts)

IronLionZion

(45,514 posts)

phleshdef

(11,936 posts)But that's turned into a denial game.

phleshdef

(11,936 posts)If you look at that particular stock's prices over the past 10 years or so, that company had stock values that weren't much different than the peak shown there in your chart.

bvar22

(39,909 posts)This chart, and the charts of all the major Health Insurance Corporations show that the smart money isn't running from them.

They believe that this Industry is a solid investment with growth potential for the foreseeable future.

The Smart Money isn't worried, and the price has more than doubled since the ACA was passed.

This positively destroys all the blather about how the ACA is going to hurt the poor Health Insurance Cartel. It won't.

phleshdef

(11,936 posts)The chart you are showing and the context you are placing it in seems to insinuate that this company in particular had this low stock price and then suddenly started peaking like crazy after the ACA passed. But if you go back another 5-10 years, its very clear that the stock for that company wasn't much less than the current peak and was only low in the first place because of the financial collapse.

It might be true that investors believe health insurance is a good investment because of the influx of customers. Its also true that the ACA isn't running private insurance out of business. But its also true that investors found health insurance to be a good investment before there ever was an ACA and the rise in this company's stock price likely would be pretty much where it is without the ACA at all, just based on looking at the past trend and taking the economic collapse and the recovery thereafter into account.

bvar22

(39,909 posts)I posted a chart that shows the Health Insurance Industry is alive, well,

making money, and that investors believe they will get a good future return for their investment money.

.. and you can take THAT to your Wall Street Bank!

You are the one trying to "insinuate" something.

phleshdef

(11,936 posts)Capt. Obvious

(9,002 posts)bvar22

(39,909 posts)It is confirmed, measured, and verified.

It is not dependent on YOU in any capacity what-so-ever.

It exists outside of YOU and YOUR interpretations, insinuations, or attempts to discredit it by attacking the messenger,

which is know as the Ad Hominem Logical Fallacy.

geek tragedy

(68,868 posts)than trying to hurt insurance companies.

Motown_Johnny

(22,308 posts)It has no space for people who will be paying less for insurance. I expect my costs to be lowered considerably. That does not put me in the 14% because I am already insured.

It also does not mention the ~3.5 million people aged 18-25 who have gained insurance simply by being allowed coverage from the policy of their parent or parents.

More importantly, the cost of health insurance was skyrocketing. It is still going up, but at a slower rate. That affects everyone. Maybe not this year, but in the long run everyone will benefit.

The chart is to narrow. It is only addressing the changeover from the old system to the new one.

DireStrike

(6,452 posts)They aren't being given free health care, just offered slightly better options and forced to pay for one of them, with money that may not exist. That has to be more than 3%.

Liberal_in_LA

(44,397 posts)Capt. Obvious

(9,002 posts)Wilms

(26,795 posts)

Starry Messenger

(32,342 posts)Big Female has some more dudes to kill before their time.