General Discussion

Related: Editorials & Other Articles, Issue Forums, Alliance Forums, Region ForumsHealth Insurance Rate Shock-California Obamacare Insurance Exchange Announces Premium Rates

http://www.forbes.com/sites/rickungar/2013/05/24/unexpected-health-insurance-rate-shock-california-obamacare-insurance-exchange-announces-premium-rates/It is increasingly clear that I had it wrong.

Yesterday, Covered California—the name given to the healthcare exchange created pursuant to the Affordable Care Act that will serve the largest population of insured citizens in the nation—released the premium rates submitted by participating health insurance companies for the three health insurance program categories (bronze, silver and gold) established by the Affordable Care Act, along with the catastrophic policy created for and available to those under the age of 30.

Upon reviewing the data, I was indeed shocked by the proposed premium rates—but not in the way you might expect. The jolt that I was experiencing was not the result of the predicted out-of-control premium costs but the shock of rates far lower than what I expected—even at the lowest end of the age scale.

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

Turbineguy

(37,364 posts)Fox News will come up with a new lie.

freshwest

(53,661 posts)

bluestate10

(10,942 posts)all levels of government. Republicans are better at taking credit for improvements they had nothing to do with and often vigorously opposed.

freshwest

(53,661 posts)

BrotherIvan

(9,126 posts)The rate they quoted was over $150 more than what I pay now as an individual (not company-sponsored insurance). Don't know where these numbers are coming from. I have to pay over half my mortgage for something I never use, and if I do try to use it, they deny the charge and I have to pay for it myself. I have a hard time cheering for more of the same.

SunSeeker

(51,658 posts)Those exchange rates are mighty cheap for CA! I currently have Blue Shield HMO coverage through my employer. I pay $1, 757.89 PER MONTH out of my paycheck for my family of 3. And that is AFTER my employer kicks in $1, 402.00 each month.

Ms. Toad

(34,086 posts)SunSeeker

(51,658 posts)

hunter

(38,325 posts)We ran out a COBRA to the bitter end, and my wife had to sign up for the state 'high risk" insurance pool which was oversubscribed. It took several months before she was accepted.

The incomplete high deductible insurance we get now through her work costs more than our mortgage, and there have been several bad years with medical problems that wiped out our savings and destroyed our credit rating.

This was all the consequence of random stuff falling out of the sky that could have happened to anyone.

As far as I can tell, insurance companies do everything they can to shed customers who become expensive.

The U.S. ought to have a national health care system like actual first world nations. Maybe this is an evolutionary step in the right direction, although I tend to think it was a Hail Mary pass to prevent the collapse of the existing health care industry.

pnwmom

(108,990 posts)for developing any new conditions or to limit annual or lifetime expenditures on you.

Politicub

(12,165 posts)That has to count for something.

And you have a really good deal to get that kind of rate on the private market. No one is going to make you change insurers, so just think of Obamacare as being there when you need it

Who is your insurer?

xtraxritical

(3,576 posts)

flamingdem

(39,319 posts)pnwmom

(108,990 posts)Have you looked into that?

Honeycombe8

(37,648 posts)so we know you're speaking truth as opposed to fearmongering.

What company quoted you? What were the terms of hte policy you were seeking? (deductibe, total out of pocket for year, individual or group or family, did it include dental and mental health, how much for Rx, what were the copays for exams and Rx, etc.).

What was your pior (or current) ins co? What are the terms of that policy? (No two policies have identical terms.)

What is your age, gender, health status, and do you smoke? If you smoke, how much do you smoke, and for how long have you smoked?

Are you in California? Is the company you got the quote from part of the exchange, that the OP article is referring to?

Only when we get the above information can we know how the ACA is affecting your premiums, or IF it is.

BrotherIvan

(9,126 posts)You want me to supply my personal medical information to you so you can judge if I'm fearmongering or lying?? Would you like me to post a copy of my medical records for your examination? Are you fucking high?

Here are the numbers, for all of you, I used to pay $185 per month before the ACA. I have Blue Cross of California that I pay independently and have kept it through the years even when I had a salaried job (most of the time I work as an independent contractor). Every 3-6 months since the insurance act passed I have received a letter that my premiums are going up until now I pay $329. On the exchange, the quote was $599 for a commensurate policy with about the same deductable. And no, the calculator did not ask any of the health questions you demanded. That is for ONE person in our two person household.

ETA: now that I have read some of your downthread replies, I don't know why I even bothered taking the time to answer. You are all over here spewing health insurance company talking points and pushing that people should be denied access to care and things like birth control because they aren't medical necessities "rates will go up". WHY do all the cheerleaders always sound like RW trolls? If the Republicans kick out the Tea Party will you please go back?

intaglio

(8,170 posts)Basically you are making a claim unsupported by any fact except your dislike of the ACA and, probably, Americans.

truedelphi

(32,324 posts)The website that was up and running about a year ago quoted that we would pay as an over the age of 58 couple living in California about 559 bucks a piece.

There would also be a $ 5,000 a year deductible, again for each of us. So that by the time we paid the premiums, 1,118 a month X 12 = 13,416 a year, plus the deductibles, we would have to spend out of pocket some 23,000 and then and only then would the insurer be required to spend a penny on us.

Oh and for what it is worth - there are co-pays!

Squinch

(50,992 posts)truedelphi

(32,324 posts)Come, has been replaced (apparently) by the website cited in this discussion.

And according to this new website, we will have as our monthly bill a mere $ 102 for the premium. No discussion about where this $ 102 a month is to come from - we don't have it. I have yet to read any article in any newspaper that says that those of us in the 17,000 to 39,000 dollar a year income range are not going to be screwed big time.

So although if the new website quoted here is true, we are only on the tab for $ 102 X 12, then I won't moan too much. Maybe I can babysit on weekends and make that money?

But what worries me is I cannot find anywhere on the new site any discussion of deductibles. And I know there are deductibles being required of almost every insurance holder - and people are really steamed about that.

So if this household still needs to come up with an annual $ 5,000 deductible a piece deductible, plus co-pays, as was detailed in the original website, we will be paying 102 a month X 12 + 10,000 + co-pays before we receive a single penny of help from a Big Insurer. Any couple making under 35,000 a year knows it isn't possible - at least not if you are paying rent at steep prices as we do here in California.

Yet the Obama/Rahm Wellpoint Heath Insurers Guarantee Program has its fans here, so I guess I should just friggin' shut up.

pnwmom

(108,990 posts)Is that all below $17,000 a year?

truedelphi

(32,324 posts)here in California, up to about 23K $$ a year. However, the last time we were able to qualify for health insurance, it had an $ 800 a month deductible. And of course, that has to do with Calif. state policies, and the consideration of rent payments being so high.

I have no idea what will happen in California after the 2014 ACA provisions kick in.

I did really like the fact that our household would have gotten help on a per month deductible basis, because if our household has to come up with a $ 5,000 a year deductible before help is given, it means we would probably be dead, since we don't have the $ 5,000. Help being offered after $ 800 as spent seemed like the way to go. (Our years of retirement money was wiped out during the bankruptcy.)

.

pnwmom

(108,990 posts)I'm truly sorry you had to go through all of that. I hope ACA improves the situation for you.

intaglio

(8,170 posts)making an unproven claim?

davidthegnome

(2,983 posts)You're attacking someone's character and credibility simply because they have a post count of under 500? Some of us who have been here for 5-8 years or more have fewer than two thousand. Are we all simply trolls then?

You clearly assert that the poster is a troll, then suggest that the poster probably doesn't like Americans... based on your differing opinions regarding the very controversial ACA... then you have the audacity to attack the poster for not having facts?

Until the ACA is fully realized - until it actually comes into effect for the vast majority of us, I will withhold judgment on it's overall value - but there is plenty of room for debate, for argument, for difference of opinion.

Personally, I think that, as people who are more left of center (generally speaking) we might want to keep "low post count members" around so that they may eventually aspire to that lofty goal of becoming "high post count members". If they are in error, well, that's why we have these "facts", which you mentioned. It would seem that you also did not use them in your attempt to refute the poster's claims.

hunter

(38,325 posts).... and we often have to fight for what we've supposedly paid for.

Our "deductible" is about $8000.

If we'd had any sense we'd have moved to a first world nation when we were young.

Oh well, live and learn.

pnwmom

(108,990 posts)for people with household incomes up to the 80K range -- since that would require knowing what a person's taxable income was?

These subsidies will be paid starting next January directly from the govt. to the insurer.

flamingdem

(39,319 posts)Like you reasonable then expensive for not great insurance. Best is to get it through an employer since now Cobra isn't an issue and the exchanges make it easy to get something if you leave or switch jobs.

That said I am unhappy with rates for 60,000 and up earners.

AllyCat

(16,215 posts)Last edited Mon May 27, 2013, 01:12 AM - Edit history (1)

I have insurance through my job that used to be good and cheap. Now, the ceo of our place is lowering options and care while increasing the deductible and out of pocket. The rates quoted here would bankrupt my family. Hope it's different for the federal exchange when it comes out. I live under Walker's rule so we get federal.

LiberalFighter

(51,029 posts)You use to pay $185 per month? I don't know what type of coverage you have that you only had to pay $185. I seriously doubt it amounted to a hill of beans.

If I had paid for my coverage back in the early 90's it would had been in the $700 to 800 range. And it was in a plan that had everyone covered at a corporation with sites across the country. I believe we had about 600,000 employees not including the retirees at the time.

flamingdem

(39,319 posts)It's crappy catastropic insurance and if you got in on it a long time ago it was good up until a couple of years ago when the increases every six months started.

Same plan now is approx. 320 ymmv

LiberalFighter

(51,029 posts)More of a supplemental like for cancer?

flamingdem

(39,319 posts)I think it was called Smart Sense or something. It just had a very large deductible - 8,000 or so. I'm ballparking but she bragged about its low cost and two free visits a year or something. They didn't take new people at that price. They did offer $230 about 1.5 years ago which is now $330 ish. For nothing much, for fear of something like cancer or an accident. So glad those days are over.

flamingdem

(39,319 posts)because I know a woman in her 50s who had it forever at that amount and then increases started.

It's catastrophic insurance, w huge out of pocket / deductible

pnwmom

(108,990 posts)would have addressed that, right?

So the question is how much you would have to pay AFTER the subsidy is accounted for. Your health insurer won't know that because it depends on the income you earn.

cheapdate

(3,811 posts)For heaven's sake. Do you think that health insurance rate ONLY suddenly began to increase in March of 2010? Health insurance costs have been sharply increasing every year at a rate much higher than inflation for more than two decades. That's one of the major reasons why Republicans and Democrats recognized it as a major problem that needed to be solved BACK IN 1992!

I've been at the same company for almost 15 years. Our insurance is with Blue Cross of Tennessee. From 1999 to 2009 my premiums DOUBLED -- from around $400 to around $800. They're almost $1,000 today. It didn't START in March 2010 with the passage of the Patient Protection and Affordable Care Act.

Rates will probably CONTINUE to rise, as they have risen steadily FOR THE PAST TWO DECADES.

Response to Honeycombe8 (Reply #21)

historylovr This message was self-deleted by its author.

JDPriestly

(57,936 posts)

onlyadream

(2,167 posts)Well visits are paid as well as 100% hospital, we pay sick visits. For our family of four we pay $425/month. Is this something only for NY?

SugarShack

(1,635 posts)Unfortunately, I live in FLA and we have some of the most expensive, just like NY.

But we don't have that plan in our state...

onlyadream

(2,167 posts)We were looking at COBRA, $1500/month with crappy, very high deductible ($3500) insurance.

SunSeeker

(51,658 posts)He is middle-aged with a pre-existing condition. This exchange will save his life.

Che Billy

(44 posts)...we had a single-payer system. What we have now is a disaster.

Politicub

(12,165 posts)The ACA isn't perfect, but millions will reap the benefit. Those who can't afford insurance will get it without cost or offset with a subsidy. Everyone will have access for the first time in American history.

Though I think you're just shoveling a load of crap to be honest with you.

Bluenorthwest

(45,319 posts)It is sad to see you dismiss that as 'not perfect'. Such a horrible injustice should create a huge reaction but those of you who are not discriminated against really don't seem to care much about what happens to others.

Politicub

(12,165 posts)You are really grasping at straws here.

Do you have health insurance, because many people who want it don't.

Now they will have access. How can this not be a good thing?

Honeycombe8

(37,648 posts)I haven't seen it. I would like to read that provision.

Comrade Grumpy

(13,184 posts)Our healthcare system is gravely distorted by the profit imperative. We need health care reform, not health insurance reform. We need nationalized health care, not this Rube Goldberg system designed to ensure profits for those fucking parasites preying off illness.

I spend more on health insurance than I do on my car payment, my house payment, or food. Not for health care. For health insurance. I give these assholes $8,000 a year, and they still don't want to pay for a shingles vaccine.

I applaud Obama for his tiny first steps, but that's all they are.

Politicub

(12,165 posts)Rates are coming in much lower than expected.

This racket, as you say, is going to mean the difference between life and death or bankruptcy and solvency for some people.

Comrade Grumpy

(13,184 posts)To the extent that the ACA improves things for people, it's a good thing. But our health care system is still fucked, and ACA doesn't really change that.

Our health care system is full of people profiting off misery. And those profits drive our costs sky high.

I have a plan:

1. No-charge health care for everybody paid for by our taxes.

2. Dismantle the parasitical health insurance industry.

3. Nationalize Big Pharma.

Politicub

(12,165 posts)But it's not the law right now. I believe we are heading in that direction. Until we get there, the ACA has a lot to like.

But for now - be happy for your fellow Americans who have needed insurance but couldn't find anyone to sell them a policy. Be happy that there are billions of dollars set aside for building health care clinics in all areas of the United States. Think of the woman that will have a lump found in her breast early enough to treat it thanks to free mammograms and preventative care.

To throw the baby out with the bath water demonstrates a profound degree of ignorance.

Plucketeer

(12,882 posts)We could BE THERE - single payer - if this president hadn't sold out to the health insurance industry. We had BOTH houses talking positive about single payer - and the president - who had touted single payer to get folks to vote for him (along with a BUNCH of other forgotten ideas) - took on the attitude: "Well, I mean, ah, IF .... single payer could find it's way to my desk - not that I think it ever will - I suppose I might maybe could sign it. But let's not be hasty here."

Yeah, t'would be HELL to end up with the horse before the cart.

DCBob

(24,689 posts)end of story.

Plucketeer

(12,882 posts)going to the pantry and seeing if there's enough existing votes for something. Hmmmm... I could be wrong, but unless it's a move to name a new post office, nothing gets done without making effort and noise. Neither of which Obama did with respect to Single Payer health care. What stellar leadership.

DCBob

(24,689 posts)for many in congress, single payer is a non-starter.. no matter how much noise anyone makes.

Plucketeer

(12,882 posts)That's more than the president did. He was elected on talk of single payer - instant stop to the wars, etc., etc. We got rights for gays. While that's important, it does nothing to help the beleagured and scammed citizenry as a whole - the 99%, if you will. I guess as a consolation prize, he's gonna give us the TPP. Then we WILL need health care - especially the expertise of proctologists.

DCBob

(24,689 posts)Plucketeer

(12,882 posts)or was everything he talked about just plays on words?

DCBob

(24,689 posts)Despite a polarized nation and a largely dysfunctional Congress, President Barack Obama has fulfilled or made substantial progress on 73 percent of the 508 promises he made when he ran for president in 2008.

Those results come from PolitiFact's Obameter, an unprecedented four-year effort to rate the president's campaign promises. The ongoing project by the Tampa Bay Times' fact-checking website reveals that Obama has achieved 47 percent of his promises, earning a rating of Promise Kept. Another 26 percent were partially fulfilled, earning a rating of Compromise.

http://www.tampabay.com/news/politics/national/president-barack-obama-kept-or-moved-forward-on-most-campaign-promises/1271440

My patience is wearing thin for arguments that suggest Obama could defy political reality -- if he only he was good enough, smart enough, or sufficiently committed.

dionysus

(26,467 posts)Plucketeer

(12,882 posts)be happy with the status quo. Don't push - don't make noise - just be happy with the insurance subsidy setup we were able to make them swallow. Only a few votes - so don't bother bringing it up again. Hell, we're just lucky to be livin' in the greatest country on the planet. SA-LUTE!

SHRED

(28,136 posts)While I agree with your idealism if implemented it would shock our economy wsy too much. The sad truth is that for-profit health and drugs are so intertwined into even retirement portfolios that a slow weaning is necessary to avoid harming millions. I think the ACA while not perfect heads in the correct direction.

KansDem

(28,498 posts)There are what I consider to be five national security issues:

1. Defense

2. Education

3. Environment

4. Energy

5. Health

These concerns should not be left in private hands.

Honeycombe8

(37,648 posts)The purpose of insurance is not to pay for anything and everything that YOU determine you want, medically speaking. It never was, and it never should be. Ins. companies paying for numerous visits to drs to tell a patient repeatedly, yes, you're having sinus trouble (duh), or whatever, is ridiculous. Paying for things people want but are not medically required, causes costs to increase (birth control pills...what most liberals wanted...but which are not medically required and is not a medical treatment....will cause premiums to go up). I'm not saying these things are not good things, but people who want these things paid for 100% often turn around and complain about health care costs. Well, you can't have it both ways.

Shingles shot is a protection not considered medically necessary. I'll be getting it, though, one day. But ins. IMO is to protect a person from catastrophic costs for treatment, and to get annual exams to catch things early (like mammagram).

If you expect an ins co to pay for everything health care related that you might want, then expect health care costs to be sky high.

Comrade Grumpy

(13,184 posts)So, fortunately, the health insurance company's bottom line wasn't hurt. They still have my $8,000 in premiums for the last year to comfort them, too.

I don't want fucking health insurance companies. I want national health care. Our health should not be a for-profit industry.

BrotherIvan

(9,126 posts)Please, enlighten us.

Squinch

(50,992 posts)I recently went through the end of life care fiasco with my mother. They kept throwing expensive and unnecessary procedures at her, even though we begged them to stop. (And just to be clear, she DID have the DNR and all the requisite paperwork that should have made that unnecessary, but we learned that those are not sufficient to override the almighty need for unnecessary medical procedures.)

We decided to transfer her to Hospice so we could take her off the machines and end the procedures. But in the ultimate catch 22, they needed a portable version of the machine she was hooked up to so we could transfer her to Hospice to take her off that very machine. But it wasn't readily available, so for 24 hours, they kept her on the machines and continued the painful procedures so they could locate a portable machine that she could be hooked up to in the ambulance to take her to Hospice so we could discontinue the machines and procedures.

One of the most frustrating and eye opening experiences of my life.

cheapdate

(3,811 posts)that is cited in every reputable, professional analysis of health care costs in the United States that significant money is wasted on unnecessary tests and procedures. This is one of many factors in the high cost of health care in the US.

But that's not really his point, nor was his point that, "the reason insurance costs are so high is because people are getting TOO MUCH care".

What he said was that insurance will NECESSARILY cost more if it must cover a growing list of routine treatments AS WELL AS the cost of major illnesses and injuries.

That is not a controversial statement, nor is it incorrect.

You somehow misinterpreted his obvious meaning.

BrotherIvan

(9,126 posts)Just so you know, birth control pills cost PENNIES to make and ARE medically necessary for many women. But I guess that is a "liberal" fact you may not get from Fox News.

Live and Learn

(12,769 posts)by allowing people to control when and how many kids they have. Birth control pills keep costs down, plain and simple. Viagra, on the other hand....

xmas74

(29,675 posts)Without them I would have already had a hysterectomy.

BrotherIvan

(9,126 posts)That's denying women basic care based on gender. It's disgusting.

I'm so glad you've found something xmas74 to help you. Health and health care is your right.

xmas74

(29,675 posts)I've heard so many say they shouldn't have to pay for bc. Without it, I would have a hard time functioning.

Response to Honeycombe8 (Reply #30)

historylovr This message was self-deleted by its author.

Squinch

(50,992 posts)RILib

(862 posts)Birth control or the birth of a baby?

noiretextatique

(27,275 posts)and insurance costs are high because they are generally for-profit businesses. they make money by denying services, some of which are indeed medically necesary. and birth control is medically required for some women.

Demeter

(85,373 posts)and what they can afford is decreased because they will be shelling out tons of money for INSURANCE, which ISN'T healthcare, and not even the promise of healthcare, but more like a lottery ticket with only an occasional winner.

With Universal, Single payer HEALTHCARE, on the other hand....you get what you pay for.

dflprincess

(28,082 posts)A lot of people will only be able to afford coverage that has out of pockets that are so high that they will still not be able to see a doctor (and the income limits for subsidies are not high enough & bear no relation to what it really costs to live.)

The big winners in this deal are the health insurance companies and the credit card companies as people will continue to use plastic to cover the medical bills they can't avoid. The number of uninsured may drop but the number of underinsured will continue to grow.

historylovr

(1,557 posts)clarice

(5,504 posts)clarice

(5,504 posts)

emmadoggy

(2,142 posts)Welcome to DU!

Scuba

(53,475 posts)... but still feel we're better with the ACA than without. Perhaps the success of the ACA will prompt further movement toward Medicare for All.

a kennedy

(29,696 posts)It's a first step and I would love single payer also.

rhett o rick

(55,981 posts)step. Are the Democrats actively working on the second step? Or is that for the next generation?

bvar22

(39,909 posts)but HOW is Mandatory For Profit Health Insurance without a Public Option

going to lead to a Publicly Owned/Government Administered, Cradle to Grave, National Health CARE Plan for every American?

My Tea Leaves say that this is only going to make the Parasitic Health Insurance Industry STRONGER,

and GUARANTEE their Profits for the Ownership Class,

every cent of which is money that will NOT be spent of actual health care.

If anything, the ACA is a Giant Step toward the Privatization of For Profit Health Care, with the parasitic For Profit Health Insurance Industry

legitimized as the ONLY Gateway to Health Care in America.

So tell me,

What is the next step that will move us toward Medicare for All?

We are going to be STUCK with this for a LONG time.

There will be NO "Fixing it Later".

The ACA actually postpones the opportunity for REAL reform for at least another generation.

dflprincess

(28,082 posts)Honeycombe8

(37,648 posts)and recognize that 59 is certainly younger than 69. ACA is better than what we had before.

southernyankeebelle

(11,304 posts)flamingdem

(39,319 posts)and not be haunted by limits and pre existing conditions

malaise

(269,157 posts)The opposite is happening

Response to Scuba (Original post)

Ed Suspicious This message was self-deleted by its author.

Politicub

(12,165 posts)And the end of exclusion based on a pre-existing condition will be consigned to the dustbin of history.

Bluenorthwest

(45,319 posts)I'm sorry, but this law excludes my family from being counted as a family. Or as a household. That's fine with you, but of course it happens to others while you get full benefits, rights, tax breaks etc.

Good for you. Congratulations! How wonderful.

Honeycombe8

(37,648 posts)Or are you perhaps talking about some individual ins. company's policies?

Politicub

(12,165 posts)Then I can't help you.

It's a platform on which to build.

Ad if you haven't noticed, the societal pendulum is swinging toward equal rights. I am part of the gay community and live in Georgia. My husband and I have seen and lived discrimination. But are you aware that because of a federal rule change coming from Obama's HHS we won't be denied visitation rights? Do you care?

And just to clarify, do you think the entire law should be null and void because you say it's discriminatory? I want to know where you stand otherwise I don't see the point in trying to have a reasonable conversation.

L0oniX

(31,493 posts)Honeycombe8

(37,648 posts)It'll be interesting to see all the, "But wait!" naysayer posts and articles, as they search for a dark lining and impending doom in the face of facts. I predict you'll see posts of "That hasn't been MY experience," and "My premium has DOUBLED solely because of Obamacare!" and "I can't even get coverage any more!" None of which will be based on facts or cite any authority or even contain enough information for a reader to discern truthfulness or bogusness.

Time will tell, of course. But this article is based on facts. Facts are pesky things. You just can't argue with them, unless you find people willing to look away from them and base a decision on fearmongering.

loyalsister

(13,390 posts)"With every passing day, the various myths, legends and lies put forward by those with a political axe to grind, TV or radio rating to be raised or vote to be purchased, are falling victim to the facts."

antigop

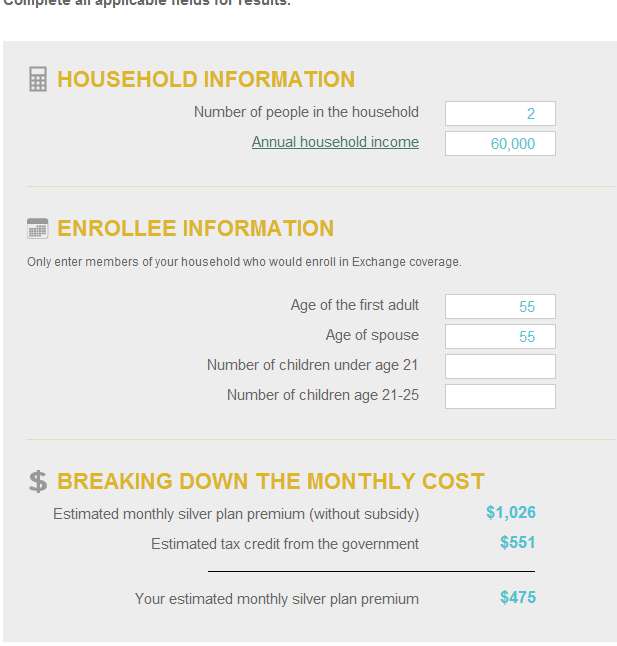

(12,778 posts)Calculator:

http://www.coveredca.com/calculating_the_cost.html

Number of people in household: 2

Annual income: 63,000

Age of first adult: 55

Age of second adult: 55

Estimated Monthly Silver Plan Premium (without subsidy): $1,026

Estimated tax credit from the government: $0

$1,026 just for premiums --- co-pays, deductibles, coinsurance are IN ADDITION to that.

Run the calculator again with same info, except age of first adult and spouse are 60:

$1249 per month in premiums -- NOT AFFORDABLE.

Comrade Grumpy

(13,184 posts)...of those insurance company executive bonuses.

...of those expensive Manhattan meals for pharmaceutical company executives.

...of paying dividends to the stockholders of for-profit hospitals.

We have to keep the parasitical grub worms fat and happy.

antigop

(12,778 posts)

woo me with science

(32,139 posts)haele

(12,673 posts)And I pay $550 a month in premiums, with my company paying twice as much. True, I have a family plan, but that only added $100 a month to my premium, and $200 to my company.

So, in total, my plan would probably cost around that much if I was carrying the entire amount myself - or more, since I wouldn't have the cost-negotiation my company does with the insurance company.

Insurance costs depends where you live, and what's required to be covered. The California Insurance market is pretty expensive (lots of people but lots of health issues), and due to the higher amount of coverage and regulations on how the insurance company can operate that the state requires (as in, it can't completely be a cut-rate no-service scam for the desperate money-making machine masquerading as "health care insurance" - they do have to provide some service...), they charge more than, say, Montana, Arkansas, or Texas.

Single payer would be far better, and eventually, California will go there.

But for now, this is the best balance between having the taxpayer pay for health-care by emergency room for a large number of people and what was available as "health care insurance" before.

Haele

antigop

(12,778 posts)haele

(12,673 posts)Not $1358. For complete coverage that has a few co-pays that are in the median of co-pay costs.

Single 63-year old making $20K a year pays only $85 a month.

Single 63 year old making $40K pays $317 a month.

And there's the federal tax credits, which I haven't figured out yet just in observation for all the categories except for single over $60K; you'd have to go into the various tables to find out what they are.

A couple, with the individual aged 63, spouse 60, and household income is over 60K does end up paying $1305 a month with a federal tax credit of $828 (for two) dropping it down to the equivalent of $475 a month (but you don't get that money until the end of the year). If the spouse is under 60, the premium goes down to $1278, but the credits drop it down to $475.

Add one dependant (child or adult) as covered under the ACA to the couple above, while the up-front premium goes up to $1533, the tax credit increases to drop the cost down to $475 a month. Add another dependent, and it drops down to $405 a month.

A couple (age didn't count when I ran the numbers) with a household income of $36K - pretty much the median income in California - pays $223 a month in premiums after the federal tax credits. Add a child, and the federal tax credits drops the premium down to $157 a month.

The federal tax credits are based on income and members in the household, not age, and are meant to balance out the difference in premiums by age and number of members covered.

Go to the link and find out - if someone is telling you it's still $1358, they're either lying about the CA exchange or they're telling you what the max the insurance companies are going to be able to offer to meet the equivalent care on the open market.

http://www.coveredca.com/calculating_the_cost.html

Now, if we aren't discussing California's plan under the ACA, I apologize for the above comment; that's the problem when there's cross-country discussions.

Having looked at "quotes" from companies, it is clear that free market costs are not affordable to the average person. This is a major problem with the ACA - however - and this is the big "however", no matter what state you live in, there is a federal tax credit in the ACA that even people who's income is up to $60K can get to offset their monthly premiums, so the 63 year old who has been quoted $1358 in a particular state is going to be eligible for some tax credits to offset that cost.

The current ACA system has subsidies and cost containment to attempt to keep medical costs below 12% of their income, which does suck, but is far, far better than what was available before, and if this is going to be an incremental step towards a single payer/rate-administration plan, it is better than what we had seen before.

Before, your only other non-employer-provided based option (disregarding eligibility for Medicare/Medicaid/Tricare/VA) was to suck it up and negotiate with an insurance agent that $1358 a month premium with no federal credits, or go for a cheaper "catastrophic" plan that didn't cover most doctor's visits or lab procedures, or wait until your health got really bad and

A) you suffer through trying to work, take care of "life business" and treat the issue yourself for a period of time until it got to be too much and you (or a family member without coverage) ended up in the emergency room - much worse off and affected for the rest of your life by something that could have been caught early with regular doctor's visits and taken care of relatively inexpensively, or

B) died younger than you would have from something that could have been caught earlier and taken care of, or

C ) ended up bankrupt from treating something in the emergency room that could have been caught earlier and taken care of.

Unfortunately, the ACA is not "health care", it's access to health care, no matter what they call it. And that's another discussion about the values of the electorate and elected lawmakers, and how those values are imposed on the citizens of this country.

Haele

antigop

(12,778 posts)That's for two people...it's clearly stated in the calculator parameters used.

NO SUBSIDIES in the example.

$1026 for two people age 55, $63,000 annual household income.

Run the calculator again, same parameters except age 63..$1358 for two people age 63.

RebelOne

(30,947 posts)you are 65 and qualify for Medicare. I have Medicare and the premium is only $105 a month.

antigop

(12,778 posts)doesn't prevent you from a financial catastrophe if you should get sick or have an accident before you qualify for Medicare.

Why would someone think that just because they are healthy today, they will automatically be healthy tomorrow?

dkf

(37,305 posts)And exceed your car payment for which you may receive no benefit whatsoever if you don't get sick.

Turbineguy

(37,364 posts)you reap the benefit of not being sick. It's an insurance pool.

But yes, if as a society we thought that being healthy was a social good then things would be different.

Politicub

(12,165 posts)Your health is your most valuable thing. The ACA will help more people be healthy.

dkf

(37,305 posts)Infectious diseases are mostly under control. It's our habits that are now killing us, what we eat and our lack of activity. And if we are too poor to eat healthily maybe its because the health premiums are eating our paychecks.

hunter

(38,325 posts)Sometimes you have an accident and they can't repair you "good as new." Sometimes you inherit a bad mix of genes. Sometimes your mom gets the flu or something while she is pregnant with you and it messes you up. Maybe chicken pox messed up your lungs before there was a vaccine. Look at most type II diabetes people, many of them are from ethnic backgrounds where certain genetic characteristics helped them survive irregular, unpredictable times of famine and bad weather, but prove harmful when high calorie food sources and adequate winter and summer shelter are available.

If the problem is as you say it is, does that mean you support a universal health care system supported by taxes and "free" to all? That would be a surprise coming from dkf...

Personally I think the health insurance industry ought to be nationalized and incorporated into some sort of single payer or entirely socialist health care system. At the same time I would examine the industry's records for evidence of malfeasance of the sort that broke existing laws and killed people. I'm sure we could find a few highly paid executives to put on trial.

Jennicut

(25,415 posts)I had no control over my pancreas deciding to stop making insulin around the around the age of 30. Some people really don't have any control over their health. Sometimes, life just happens. Most of us with autoimmune diseases feel like our bodies betray us. If I had millions , I would poor it into research on autoimmune diseases like type 1 diabetes, celiac disease, lupus, scleroderma, MS, etc. There really is no reason people get these diseases aside from some of it being genetics.

CountAllVotes

(20,877 posts)I agree with your statement. I also strongly believe that many of these diseases such as the ones you name are from living on a very sick planet.

It is these same individuals that find relatives with the same problem(s).

For it are these people and their relations that are indeed experiencing the pain of the earth.

Sad, sick world. Many are dying too soon. Unexplainable in many cases ... rapid onset and sudden death.

And there is nothing that can be done or will be done for one reason:

BIG PHARMA makes loads off of these people. What does medicine do for them other than experiment? Nothing much otherwise ... no help or anything reasonable like that!

and ...

Who cares as long as the conditions that you mention exist? They are not contagious, so forget these losers eh?

dkf

(37,305 posts)We just don't understand it yet. The way we've bastardized the production of food, and the amount of anti-biotics in the food chain are playing havoc with our auto immune systems.

I keep telling people I wish we would be putting a whole lot of research into medicine instead of paying so much for our health care system. Only a government that needs to pay for health services sees an advantage in solving diseases whereas any for profit corporation's wet dream is a lifelong customer that will LOSE HIS LIFE if he can't pay for their services.

I see things like this: Engineered Gut Bacteria Reverse Type 1 Diabetes in Experimental Mice

http://www.genengnews.com/gen-news-highlights/engineered-gut-bacteria-reverse-type-1-diabetes-in-experimental-mice/81246608/

Then I see things like this: Fecal Transplants: The FDA Steps In

http://www.wired.com/wiredscience/2013/05/fecal-transplants-fda/

I'm not sure I trust the US Government to do this properly either.

Scuba

(53,475 posts)

drm604

(16,230 posts)Yes, some are to blame for their health problems but many, possibly most, are not.

I am not to blame for the chronic problems that hit me at 15 and have plagued and impoverished me my whole life. At that age I did not drink or smoke (and still don't) and I was physically active.

MannyGoldstein

(34,589 posts)That's actually been demonstrated many times, yet the diet scolds won't stop their "common sense" (i.e., unproven) scolding to eat less salt. So people get unhealthy by trying to get healthy.

Same goes with weight, fat and meat consumption, and all kinds of other stuff. Lots of scolding, little evidence.

"God heals, the physician takes the fees" - Ben Franklin

BrotherIvan

(9,126 posts)All the shills on here have no idea what they're talking about. They are obviously not Californians but just want to jump up and down and push the latest cheerleading line. It's pure crap. These rates are not only not affordable, they are ridiculous. And according to the cheerleaders on here, you shouldn't use that insurance either for things like visits to the doctor or birth control because then the rates will go up.

So we're all supposed to be so happy we are paying thousands per year to predatory companies for something we can't use! The ACA may improve some small things but it still traps us in the most broken healthcare system in the modern world.

Skittles

(153,174 posts)imagine the price after a few years

LWolf

(46,179 posts)flamingdem

(39,319 posts)antigop

(12,778 posts)those aren't my statistics --- I'm just pointing out how unaffordable the premiums are.

flamingdem

(39,319 posts)It's better for those earning less. It is much better insurance of course but if one doesn't use it, my case, then it's too expensive still.

bummer.

antigop

(12,778 posts)They will feel they are getting stiffed when other people are getting insurance much cheaper.

flamingdem

(39,319 posts)Maybe they should have been more vocal during the process.

I clearly remember those with work insurance not giving a crap about people who were struggling with insurance.

Republicans mostly, but some dems too

antigop

(12,778 posts)They will not have affordable insurance.

OKNancy

(41,832 posts)you are trying very hard to pour cold water on the very real benefits of the ACA.

antigop

(12,778 posts)If you get laid off in 2013 and have no income in 2014, you have to come up with the premiums for 2014 WHEN YOU HAVE NO JOB.

BuelahWitch

(9,083 posts)What happens if you lose a good paying job you had the year before and you have to take a job that pays much less. Are the premiums going to be adjusted for emergencies or will we be stuck until the next year?

Godhumor

(6,437 posts)In which case, current situation takes precedent over previous. In other words, no, you don't keep paying your previous while employed premium.

antigop

(12,778 posts)She/he may have to retire due to no job prospects. Some people do get pensions and may start receiving them.

antigop

(12,778 posts)OKNancy

(41,832 posts)We will save about $500.00 per month

antigop

(12,778 posts)That's just for premiums --- for the silver level... You have to pay copays/coinsurance/deductibles in ADDITION TO THE PREMIUM if you require medical attention.

You have to look at the max out of pocket in addition to the premiums.

woo me with science

(32,139 posts)

dumbcat

(2,120 posts)That poorer people would finally have medical insurance, and the better off would have higher premiums to cover them? Isn't that what a progressive system is supposed to do, or am I missing something?

antigop

(12,778 posts)Flatulo

(5,005 posts)qualify for heavy subsidies will be spending half their after-tax income on health insurance, and only if they're not unfortunate enough to get sick. If they get sick, the copays will wipe them out.

Turbineguy

(37,364 posts)when you don't catch some disease because somebody near you could not afford to see a doctor. This is not like a casino.

woo me with science

(32,139 posts)The whole purpose of the ACA was the mandate. It was a fucking scam to entrench the bloodsucking health insurance middlemen into our health care system and ensure that every single American is forced to feed their racket.

The people defending this are the very same people who defend every single outrage by the corporatists who have hijacked this country. They defend indefinite imprisonment of human beings without due process. They defend slaughter of innocents by drone and the President's ability to murder at will. They defend austerity budgets and cutting critical social safety nets. They defend corporate authoritarians in our schools, and they defend sending our jobs off to other countries. They defend ANYTHING that benefits the one percent. They spend their time at this site insulting and lecturing "liberals" and spewing right-wing talking points. They are not Democrats, except in name.

They are a cancer in our party. Our party has been hijacked by Wall Street, and they pay good money for constant, insulting propaganda to tell us that the siphon in our pockets is a GOOD thing.

How long do we tolerate this garbage? How long?

antigop

(12,778 posts)hunter

(38,325 posts)Ask any "uninsurable" person who has no health insurance, anyone who has faced a COBRA they can't pay because they are too sick to work, or anyone who has run out a COBRA.

As wretched as this is, it's an improvement.

Sometimes the difference between a "F" and a "D" grade is important.

I give "Obamacare" a "D-" but that's a marked improvement from the "F-" kill it with fire our existing healthcare system deserves.

The most remarkable thing about healthcare in the USA is that even people with excellent insurance and/or wealth can get incredibly inappropriate, expensive, and sometimes deadly health care. Sociopathic doctors who are only motivated by money are going to target the very wealthy; you are much less likely to find them working the local free clinic or middle class HMO.

woo me with science

(32,139 posts)Last edited Mon May 27, 2013, 02:32 PM - Edit history (3)

They will fix it later. This is the mantra we are always fed. But the promised "fixes" and "improvements" NEVER happen.

You have to understand what has happened here. We did not get this "D-minus" plan because nothing else was possible. At the time of the negotiations, the country polled heavily in favor of a public option. It would not have been difficult to rally the country to pressure for something better than this, if Obama and corporate Democrats had wanted to do so. It would not have been hard to design a plan that focused on the aspects of health care delivery that REALLY needed fixing: cost control. They didn't. Obama did not fight for a public option. There are no serious cost controls in this plan, and there never were, which is something that does not happen accidentally. Obama chose to make backroom deals with the health insurance companies, because this administration is corporatist and has been corporatist since the day they got into office. If you tune out all the propaganda and simply look clearly at what is being DONE, over and over again, you will see that what we got was entirely consistent with every other decision this administration has made in the corporate arena. The corporate Democrats did not push for something better, because what we got was precisely the goal: a sop for the One Percent.

We are on a road of austerity budgets and Social Security cuts. We are on the road to privatized schools. We are on the road to the Keystone pipeline. We are on the road to the Trans-Pacific job and wage killing agreement. And we have a brand spanking new health insurance program that mandates the purchase of an obscenely overpriced product that vast numbers of Americans still will not be able to afford to use.

They are not working on our behalf. That is a truth that people need to get their heads out of their nether regions and face. We have a broad, systemic problem of corporate money in our government and in our elections, and both parties are working for corporate interests, not ours. This plan is an ironically named insult to and assault on Americans. There is no serious affordability here at all, nor any serious plan to provide affordability, and there never was. The point of the plan is, was, and has always been The Mandate: a captured market for an obscenely overpriced corporate scam of middlemen and thieves.

hunter

(38,325 posts)They've cut in half the straw that will break their camel's back.

It's a temporary patch.

The machines they have built become brittle.

CountAllVotes

(20,877 posts)I'm glad I'm not alone in my thoughts regarding this enormous pig of a scam that only the very few, the desperate ones, will find themselves to be the final victim of in the end.

It reminds me of so many other things I'm seeing these days, from long-term care plans that some of the wealthier folk out there have been paying for and all of a sudden, it goes insolvent with doubled premiums, alas becoming un-affordable for them as they age. File a class-action lawsuit they propose? WTF? Why don't they DO SOMETHING? Some have been paying into this SCAM for as long as 30 years only to find they are shyte outta luck on this deal -- perhaps $40K in the hole on this "deal" ... a "deal" for those that could afford it, yes even they too are beginning to feel that little *pinch*.

This is but ONE example of how many other scenarios just like this?

Same thing here is the way I see this new B.S. deal. A lot of $$$ for what exactly? And, pray tell, what if you don't have that 1K a month for "it", whatever "it" is?

Fact is, I don't trust these suckers one damn bit and it is a treacherous pig of a scam I must agree.

Greed rules and Wall Street and the corporations are the thankless masters of we the servants of the United States of America. Don't you just love this unique form of dare I say it ... FASCISM?

Bozvotros

(785 posts)Living in America under Obama is a little like being an abused spouse who sheds her psychopathic mate and marries someone who no longer punches her in the face and molests her children. At first you're happy things aren't so brutal. You don't even care that he told you a lot of lies and hangs out with some of your ex's old friends. And, OK, sure, he fenced some of your jewelry for meth and booze and new clothes but he talks so sweet to you.

Believe me, I am not someone who thinks it would have made no difference if we would have elected McRomney or any other stooge the Repugs would have run. With the Pugs in the White House and the House and kind old Harry Reid standing between us and full fascism, I am giving the nod to fascism 10 to 1. But Obama has continued to disappoint and finally really irritate me. I am sick of having to compromise and capitulate to these sick fucks running the con game that is American politics. I am tired of being told to wait for things that should have come long ago or that this screwing is less harsh than the one we could have got or that something is better than nothing.

We are at war all right but it isn't with Al Qaida and the Muslims. (Good band name... I doubt it is taken.)

lhooq

(35 posts)how affordable the PPACA is. For me (income < 100% FPL, residing in Florida, a state not expanding Medicaid), health insurance is as unaffordable as ever and that won't change any time soon. No subsidies for me, because I make too little!

Anyway, woo me with science makes a cogent argument that the PPACA entrenches the for-profit system and that that's the main intent of the law. One point not said but I'll say it: from where did the individual mandate originate? From the Heritage Foundation, in the early 1990s, as part of their response to the Bill and Hillary Clinton health plan proposed in '93. Go figure.

Skittles

(153,174 posts)

ohiosmith

(24,262 posts)AUTOMATED MESSAGE: Results of your Jury Service

At Mon May 27, 2013, 09:30 AM an alert was sent on the following post:

No, it's not affordable. It's a fucking racket.

http://www.democraticunderground.com/?com=view_post&forum=1002&pid=2905411

REASON FOR ALERT:

This post is disruptive, hurtful, rude, insensitive, over-the-top, or otherwise inappropriate. (See <a href="http://www.democraticunderground.com/?com=aboutus#communitystandards" target="_blank">Community Standards</a>.)

ALERTER'S COMMENTS:

The whole purpose of the ACA: "It was a fucking scam" "the President's ability to murder at will." Anyone who supports the ACA is a "cancer in our party".

What the fuck? Is this really Democratic Underground? When you go so far beyond constructive criticism that you start posting freeperish attacks on a sitting Democratic President, the Democratic party, and members of DU...maybe it's time to take a break. This is incredibly over-the-top and inappropriate.

You served on a randomly-selected Jury of DU members which reviewed this post. The review was completed at Mon May 27, 2013, 09:40 AM, and the Jury voted 2-4 to LEAVE IT.

Juror #1 voted to HIDE IT and said: No explanation given

Juror #2 voted to LEAVE IT ALONE and said: No explanation given

Juror #3 voted to LEAVE IT ALONE and said: It's not a "freeperish" attack. It's a left of center attack that embodies the opinion of many Democrats. Leave the post.

Juror #4 voted to LEAVE IT ALONE and said: Not only is there nothing wrong with the post per DU's Community 'Suggestions' it is also agreed with by many members here. You don't like their points? Tough... they are totally valid.

Juror #5 voted to HIDE IT and said: Language is inappropriate and verbally abusive to fellow Democrats.

Juror #6 voted to LEAVE IT ALONE and said: Many in the party have concerns about ACA -- though admittedly not to this degree. I don't think this rises to "hide" level.

Thank you very much for participating in our Jury system, and we hope you will be able to participate again in the future.

Flatulo

(5,005 posts)The first year the rates weren't too bad, but still high. For the next few years we saw shocking increases. Unless you're destitute with no income, in which case you'll qualify for a fully subsidized Commonwealth Care plan, these policies will consume 50% or more of your after tax income. When you add in the copays, there's nothing left to live on.

Health insurance is bankrupting us. It's only going to get worse.

lhooq

(35 posts)Reading

fills me with envy.

In contrast, with the PPACA, if you're destitute, then you're supposed to be picked up by expanded Medicaid. But many states, including big ones like TX and FL, are not expanding Medicaid. Thus, if you are destitute, well then you better hope to get on hospital charity care, use the county health department, or figure bankruptcy is how you will discard any large medical bills. Romney's Commonwealth Care plan does not sound that bad, after all.

Hey, I'm just joking, well, sort of ...

Journeyman

(15,037 posts)OKNancy

(41,832 posts)I went to your link and put in your figures... You left off some important information.

[URL= .html][IMG]

.html][IMG] [/IMG][/URL]

[/IMG][/URL]

Editing to add: I just read that the income is adjusted gross income.... $475.00 per month for a couple with an adjusted gross of $60,000 is doable under almost any circumstance.

antigop

(12,778 posts)haele

(12,673 posts)The difference is that you now are netting after taxes over $4100 a month, and the electorate feels that you're now making enough to handle paying up to a quarter of your monthly net income on health care and not hurt to much, because you can still deduct half of those costs on your income taxes when they're due.

You should be able to get back as much as $6K a year on your taxes above that amount. It's not right, but that's what they thought they could promote just to get 40% of the citizenry at the lower economic scale out of emergency room health care.

I would have rather seen them put the drop-out at $90K - especially in California, where people can be attempting to pay off both student loans and mortgages up to $3500/$4000 with a net of $5500 a month of income.

So, the upshot is that if your household income is under $63K, the ACA is much cheaper than anything you can get on the market. After that, you're stuck with market costs.

I'll agree, it's not comfortable for those who have a household income around or above $63K; but luckily for some in that category, if you have a dependent (which adds significant costs to a household) you do get the tax credit applied.

It's very affordable for those who are on the margins, who are eligible for EIC, and who don't usually have a job that gives them health coverage.

Unfortunately, a lot of us - probably around 10% of this country - who are just above that line, but not well-off enough that $1K a month is disposable income, it still stings.

But this is what it comes down to for me:

Single Payer - vs. - Health insurance/health access plans/ACA -vs.- Health insurance/health access plans with no ACA in place.

It's not "ACA" vs paycheck. It's access to health care that doesn't depend so much on the whims of insurance companies and the cost is somewhat regulated more fairly.

What I pay now in a health-care premium from my employer-provided insurance for just me and my spouse (if we were both 55) is 2/3 the cost of what it would be under Covered CA, and our Aetna plan is considered comparable to most.

If we were both 55 and had a household income of $63,000 right at, the CA plan would be only $300 a month more than what we pay now, and give us the same benefits we have now.

If I lost my job, I would have to come up with over $1450 a month while on unemployment or doing part-time work to pay for COBRA to keep a continuance of a comparable insurance we have now until I could get another employer-provided insurance plan - if they had one.

Right now, we would be paying significantly less between the CA plan/my employer's plan with up to a household income of $62,000. Frankly, if I wasn't so close to the 55 age level, and our combined household income wasn't well within $10K of the upper level with a potential to go up this year, I would definitely consider going with Covered CA for ten years or so vice the employer plan and hope to transition into single payer that way. If I didn't have health care, I'd go ahead and suck it up.

I've gone the emergency-room health care plan route in the past, and as I get older, there are more things going wrong; I can afford the bills I have now, I couldn't if I didn't have health insurance to cover most of the costs I'd be facing without it.

So I see it this way - if I had to, $1K a month in premiums is cheap when the insurance company is "negotiating down" an additional monthly average of $2400 in medical costs due to chronic problems (some thanks to that period of "emergency room health care", others due to age).

Last year without health insurance, out of pocket for both me and my spouse would have been $57,653 for basic treatment of chronic health issues.

Not counting any of the emergency/urgent care visits - which came up to an additional $80K plus, according to the statements from my insurance company. $10 for an anti-nausea pill. $112 for an IV rig. $75 for the CNA to draw blood. $700+ for labs (bills for which kept coming in for 3 months afterwards) $1,200 for a 2-hour "room" stay at the Urgent Care. $220 for the follow-up doctor visit.

The main problem with the ACA and all of the exchanges is that it isn't single payer. And so, we get hung up on the term "affordable" - which single payer would be marginally more so.

The hope is that, like Social Security and Medicare, is that the ACA builds a framework to become a single payer or cost-regulated system that is truly affordable and mostly out of hedge fund manager and CEO hands.

And honestly, as bad as it might look now, it looks as if this hope is possible - especially as these state exchanges will work for the majority of their populations.

Haele

antigop

(12,778 posts)Well, you know, what she says. Nice try.

This will be unaffordable for lots of older pre-Medicare people who do not qualify for subsidies.

haele

(12,673 posts)I can wait, I have insurance through my company. At least for the next three years or so.

Scrap it all, spit in the eye of the people who run the insurance and health care lobbies.

I don't care about myself, I can be a martyr - I'm not afraid to die (I am afraid of being disabled, though), I've done without health care at times in my life, been living in a van eating raman noodles poor before, and don't mind at all if I become crippled or develop something undetected because I've got all my quarters for full disability and a number to a disability lawyer if I need it. Now that I'm 50+, even less of a problem...I can wait until I start collecting early SS and Medicare, so long as they haven't f**d that up.

That's me.

Of course, I'll say the above until I get laid off, and am stuck with a truly un-affordable COBRA plan ($2K+ a month just for myself and my chronically ill spouse, $3K if we add the dependent grandchild that's covered under my current health care, as of 2011 when I last sat down with the benefits person).

Choose between $2K - $3K a month on the market or what the ACA gives me and my household - $1200 a month, $515 a month if we can include the grandkid. Guess what I choose?

Now that it's "We" instead of "Me" - What we had before ACA was un-affordable to me and to anyone else who was taking care of someone with serious or chronic health problems.

My disabled spouse can't go without health care, and neither can my stepdaughter (dependent under 25) and her baby (the other dependent) that we have custody of.

Nor will most of my neighbors, now lining up to sign on to Covered CA, who will go back to hoping not to get sick and treat themselves with OTC's until they have to go to the emergency room.

I know the for-profit health care system in this country sucks any number of scatological body parts.

I'm just happy some people who didn't have access to anything other than emergency room health care now have access to health care.

I'm pissed it's not single payer, that it doesn't make health care affordable for all of us, but at least some people will get it, and perhaps not die of undiagnosed cervical cancer in the emergency room before she's 55 and leave three kids and a husband, the way the working family across the street from me ended up last year.

You see, it's all about the hostages to fate, the family members, and how many hostages people are willing to give up. If I didn't have anyone that needed health care, I'd probably be just as strident about the financial/medical death panels and the incremental destruction of the middle class.

"How dare they call themselves affordable charging a couple over fifty-five $1300 for health care...." Really, they should have called it "Regulated Health Care Access Act" and stopped pretending to be affordable. It's not affordable (compared to Medicare?) if you have a pre-tax household income of $63K a year and/or are midway through 50 - which is about 25% of California.

I know they're playing one level of the working class people against the other. It's Jay Gould all over again. "I can hire one half of the working class to kill off the other half"...

We can do better, and I'm looking long out - hoping a very flawed ACA is just part of the incremental process that will be revised and re-tooled, just like Social Security, just like Medicare, just like the VA, just like all the other programs that go up and down depending on the whims of the electorate.

We've also got a really shitty value system in this country where people are judged on the money they make, and until we as an electorate take to the streets to change that, and take back the media in the process, we're not going to advance beyond where we are now, where those with the most money get to play gotcha with those with less, and turn us each against the other.

Got a problem with the ACA - vote. Agitate. Push. Move to change the morals and values of this country.

Because there are serious gaps, because it doesn't benefit you and me (except in extremis) it needs to be re-tooled. So many good programs over the years - education, civil rights, health care, financial reform - died because they were scrapped for being politically imperfect, a waste of time and money, instead of being re-tooled to fit the problem they were addressing.

Haele

antigop

(12,778 posts)retirees and workers who have to purchase off the exchange and don't qualify for subsidies.

And they are going to be livid when they find out how badly they are getting screwed when they see how much cheaper the rates (with subsidies) are for other people.

You can try and spin this all you want, but ACCESS means nothing if you can't AFFORD it.

dflprincess

(28,082 posts)and a maximum out of pocket of $6,400 for a single, $12,800 for a family.

The "Platinum" plan has no deductible but still has a max out of pocket of $4,000 (single) and $8,000 family.

The Gold plan has no deductible but the out of pockets are still $6,400/$12,800.

The Bronze plan has a $5,000 deductible and the out of pockets are $6,400/$12,800.

I can't find anything that calculates the premiums for the Bronze, Gold or Platinum plans.

http://www.coveredca.com/PDFs/English/CoveredCA-HealthPlanBenefitsComparisonChart.pdf

No word on how any of these plans will actually improve access to care when you can't afford the out of pocket.

antigop

(12,778 posts)premiums and/or you can't afford to get sick.

Thank you.

dflprincess

(28,082 posts)I can only guess that they have really, really good insurance or enough cash to cover all their out of pockets.

antigop

(12,778 posts)

Ruby the Liberal

(26,219 posts)That is about HALF the cost of my monthly COBRA in 2009, and about half of what Vermont is estimating for their exchange.

Calculator: http://www.coveredca.com/calculating_the_cost.html

flamingdem

(39,319 posts)and that is a problem.

Ideally it will lead to lower rates in the future for everyone

Ruby the Liberal

(26,219 posts)and showing how it can work in practice.

My state is going with the Fed exchange to start. I call that a victory over the GOP when GOP states defer to the fed on this.

flamingdem

(39,319 posts)through work most of the time.

If a single makes a low end salary 20-30 that's a sweet spot for subsidies - 85 a month and great coverage.

However 50-60 grand makes the monthly more than what I was paying, catastrophic but since I rarely use it.. my issue is cost. I can't pay $500 a month. Just on principle, I'm tired of those rates when I rarely use it.

antigop

(12,778 posts)antigop

(12,778 posts)flamingdem

(39,319 posts)hide income if they are independents

antigop

(12,778 posts)See example:

http://www.democraticunderground.com/10022905392

antigop

(12,778 posts)Run the scenarios on the calculator

Each will pay $411 -- no subsidy.

Once you reach $46,000 the subsidies go away and the premium stays at $411 for a 50 year old regardless of income above $46,000.

Indykatie

(3,697 posts)Is it Perfect? No but it's a great start. The combination of the subsidies and elimination of pre-existing limitations along make this a huge win for many. The unlimited preventive care paid at 100% coupled with no cost contraceptives makes ACA very attractive especially to women. These basic features will be found in all the Exchange plans under ACA. Many companies such as the one I work for have already implemented many of ACA provisions such as children covered to age 26, unlimited preventive care, free contraceptives and unlimited lifetime benefits. Those who continue to whine and complain about the ACA and claim to see no good in the law are either totally uninformed or just out to troll in my opinion. Many of the complainers would never accept anything less than Single Payer and that's an unrealistic benchmark. ACA will also force Employers to cap contributions for their plans to a level required by law. I urge everyone to go to an independent site such as the Kaiser Foundation (KFF.org) and educate yourself on the provisions of the ACA so you will know when you are being fed misinformation including erroneous statements being made here on DU where I would expect commenters to have a better grasp of the legislation. My big worry is around implementation. I worry that some States will not feel motivated to get it right preferring instead to have something else to criticize the President about.

antigop

(12,778 posts)antigop

(12,778 posts)nt

ProSense

(116,464 posts)"$1026 per month for two people w/ income $63000 IS NOT AFFORDABLE."

...spreading misleading information.

The fact is the premium you're citing is based on the age rating and doesn not apply to any couple earning $63,000. There are also other factors to consider.

http://www.democraticunderground.com/?com=view_post&forum=1002&pid=2905988

ProSense

(116,464 posts)"Should a 50-year-old w/ $46000 income pay the same as a 50 yo making $500,000?"

...that's what happens now because anyone not eligilbe for Medicaid has to pay the same as someone earning $500,000.

The ACA changes that and makes the wealthy pay more via additional taxes on ordinary and investment income.

http://www.democraticunderground.com/10022078875

slipslidingaway

(21,210 posts)remember two thirds of medical bankruptcies were people who had insurance.

You never know what happens when a serious illness makes an appearance.

Scuba

(53,475 posts)slipslidingaway

(21,210 posts)it will help some people receive care no doubt, but many people will find that having insurance can come at a high cost. Two-thirds of the medical bankruptcies were people with decent insurance.

Scuba

(53,475 posts)madville

(7,412 posts)These are all 60/40, 70/30, 80/20 type plans, the family out of pockret annual cap is around $12,000, who has that laying around?

antigop

(12,778 posts)if you need medical attention.

slipslidingaway

(21,210 posts)for the past few years. You can maybe do this once or twice, but after awhile it takes a toll.

slipslidingaway (1000+ posts) Send PM | Profile | Ignore Wed Jun-30-10 09:11 PM

Original message

If you have HC insurance what is your annual out of pocket maximum?

Ours is over 11,000 and that differs from the annual deductible which is about 2500.

http://www.democraticunderground.com/discuss/duboard.php?az=view_all&address=389x8667267#8667333

hue

(4,949 posts)that ever happened to the US folks!

The Repukes fear success for our President & the Dems.

madville

(7,412 posts)I imagine family rates will be $800-1200. That's for the Silver plan which is 70/30, the insurance pays 70% of the bill and the insured pays 30%, anything major will still throw most people into medical debt.

antigop

(12,778 posts)in addition to the premiums.

hunter

(38,325 posts)Maybe I end up living on the streets but I pity those poor under-paid drones at the collection agencies.

Sorry, I've got no money today and my credit rating is in the toilet. Now what?

antigop

(12,778 posts)The interpretation, which was released by the Internal Revenue Service (IRS) late last month in the form of a proposed rule, related to the “Employer Shared Responsibility Provision” of the ACA, popularly known as the employer mandate. That provision provides that larger employers (those with more than 50 employees) offer insurance coverage not only to their employees, but to the “dependents” of those employees as well. If these employers fail to offer “affordable” coverage, they may be subject to monetary penalties.

But the IRS’s definition of dependents in the proposed rule excludes the spouses of employees, regardless of whether the spouse is employed.

antigop

(12,778 posts)Benefits advisers and insurance brokers—bucking a commonly held expectation that the law would broadly enrich benefits—are pitching these low-benefit plans around the country. They cover minimal requirements such as preventive services, but often little more. Some of the plans wouldn't cover surgery, X-rays or prenatal care at all. Others will be paired with limited packages to cover additional services, for instance, $100 a day for a hospital visit.

Federal officials say this type of plan, in concept, would appear to qualify as acceptable minimum coverage under the law, and let most employers avoid an across-the-workforce $2,000-per-worker penalty for firms that offer nothing. Employers could still face other penalties they anticipate would be far less costly.

It is unclear how many employers will adopt the strategy, but a handful of companies have signed on and an industry is sprouting around the tactic. More than a dozen brokers and benefit-administrators in 10 states said they were discussing the strategy with their clients.

"There had to be a way out" of the penalty for employers with low-wage workers, said Todd Dorton, a consultant and broker for Gallagher Benefit Services Inc., a unit of Arthur J. Gallagher & Co., who has enrolled several employers in the limited plans.

Pan-American Life Insurance Group Inc. has promoted a package including bare-bones plans, according to brokers in California, Kansas and other states and company documents. Carlo Mulvenna, an executive at New Orleans-based Pan-American, confirmed the firm is developing these types of products, and said it would adjust them as regulators clarify the law.

woo me with science

(32,139 posts)

nadinbrzezinski

(154,021 posts)But those workers have no care otherwise, or an emergency room

This is the half fix hunter alluded to. The system will still collapse...so either they fix it...(in this political environment not very likely) or it collapses.

There is a third way...the strikes in those sectors become national, the unions get members, and healthcare (as in good health care) is part of it.

I feel it in my bones, the bed the elite is feathering will not end well for them.

antigop

(12,778 posts)antigop

(12,778 posts)Some people will get advantages, a lot won't due to loopholes and corporations trying to get by on the cheap.

The ones who come out ahead won't have a lot of sympathy for those who are disadvantaged.

It's a classic "I got mine -- screw you" attitude.

And it was played perfectly...that's why I don't share your optimism.

cbdo2007

(9,213 posts)Companies who offer bear-bones plans will have to pay more to compete with bigger companies, or even better, it will begin a trend away from our employers offering health insurance as part of the package for regular people and put everything on the exchanges.

antigop

(12,778 posts)cbdo2007

(9,213 posts)antigop

(12,778 posts)cbdo2007

(9,213 posts)coffee and talk it over with your dinner party friends this weekend and maybe it will make sense to you in some divine enlightenment.

antigop

(12,778 posts)cbdo2007

(9,213 posts)on the computer there and maybe that will help point you in the right direction.

Happy to help Bro!

antigop

(12,778 posts)cbdo2007

(9,213 posts)antigop

(12,778 posts)understand what it is saying.

cbdo2007

(9,213 posts)to reread my post or continue to misunderstand it as well. OMG, what if we both reread and now understand what the other is saying, but we'll both still be on opposite sides. Far out man!

antigop

(12,778 posts)cbdo2007

(9,213 posts)I hope your time misinterpreting my post was well spent.

antigop

(12,778 posts)cbdo2007

(9,213 posts)antigop

(12,778 posts)nt

cbdo2007

(9,213 posts)to your post.

Good day Sir!

WorseBeforeBetter