| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » General Discussion |

|

| DaveinJapan

|

Thu Jan-27-11 08:31 AM Original message |

| Looking for help with the facts about Social Security (insolvency, etc...), any help appreciated! |

| Printer Friendly | Permalink | | Top |

| Lochloosa

|

Thu Jan-27-11 08:35 AM Response to Original message |

| 1. Try this site. |

| Printer Friendly | Permalink | | Top |

| DaveinJapan

|

Thu Jan-27-11 09:15 AM Response to Reply #1 |

| 3. Got any site that doesn't suggest raising taxes? lol...nt |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jan-27-11 09:25 AM Response to Reply #3 |

| 5. Here are some potential solutions from AARP study & CBO. |

| Printer Friendly | Permalink | | Top |

| Godhumor

|

Thu Jan-27-11 08:49 AM Response to Original message |

| 2. The SSA's annual Trustees' Report is right from the horse's mouth |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jan-27-11 09:23 AM Response to Original message |

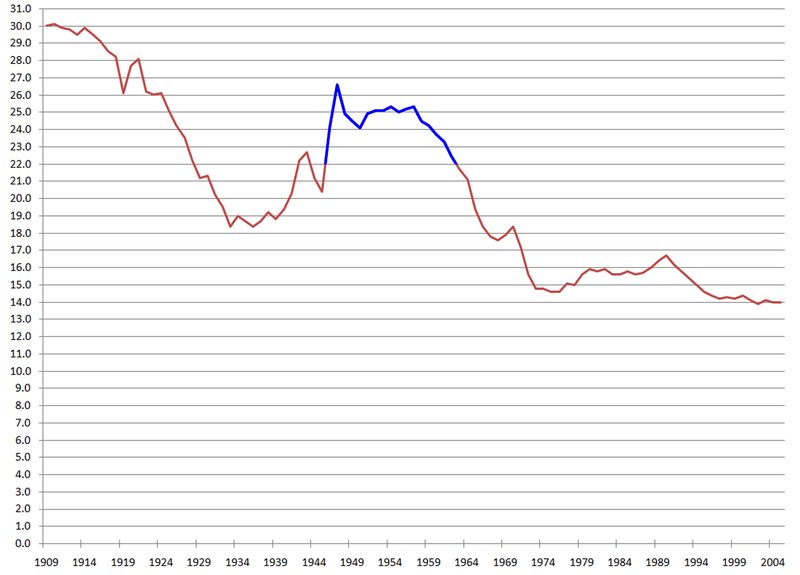

| 4. Graphic that sums it up from trustee report |

| Printer Friendly | Permalink | | Top |

| SlimJimmy

|

Thu Jan-27-11 09:50 AM Response to Original message |

| 6. I keep hearing that there is a surplus of more than 2 trillion, and that this will |

| Printer Friendly | Permalink | | Top |

| dixiegrrrrl

|

Thu Jan-27-11 10:17 AM Response to Reply #6 |

| 8. The "surplus is on paper, it is a book keeping IOU. |

| Printer Friendly | Permalink | | Top |

| lumberjack_jeff

|

Thu Jan-27-11 11:36 AM Response to Reply #8 |

| 21. So are $100 dollar bills. |

| Printer Friendly | Permalink | | Top |

| SlimJimmy

|

Thu Jan-27-11 03:36 PM Response to Reply #8 |

| 30. Well, that's not what the previous reply said. So which is it? Is the money physically there |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jan-27-11 10:21 AM Response to Reply #6 |

| 9. No both are telling the truth. |

| Printer Friendly | Permalink | | Top |

| lumberjack_jeff

|

Thu Jan-27-11 11:41 AM Response to Reply #9 |

| 22. The social security system is still in surplus. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jan-27-11 11:56 AM Response to Reply #22 |

| 23. Deficit & Surplus refers to current year changes not standing balances. |

| Printer Friendly | Permalink | | Top |

| lumberjack_jeff

|

Thu Jan-27-11 12:08 PM Response to Reply #23 |

| 24. Here's a better analogy |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jan-27-11 12:13 PM Response to Reply #24 |

| 25. Prior years balance are never added to revenue to inflate revenue. |

| Printer Friendly | Permalink | | Top |

| lumberjack_jeff

|

Thu Jan-27-11 12:34 PM Response to Reply #25 |

| 26. My first hand experience is limited to 12 years municipal budgeting. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jan-27-11 12:37 PM Response to Reply #26 |

| 27. " Your Clinton surplus example shows that, unofficially at least, they do." |

| Printer Friendly | Permalink | | Top |

| lumberjack_jeff

|

Thu Jan-27-11 01:07 PM Response to Reply #27 |

| 28. You misunderstood the last sentence. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jan-27-11 01:17 PM Response to Reply #28 |

| 29. Sadly that is kinda what Ron Paul is doing. |

| Printer Friendly | Permalink | | Top |

| Tippy

|

Thu Jan-27-11 10:09 AM Response to Original message |

| 7. Senator Sanders answers a lot of quesitons |

| Printer Friendly | Permalink | | Top |

| doc03

|

Thu Jan-27-11 10:37 AM Response to Original message |

| 10. I don't think it is just a coincidence this Congressional report |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jan-27-11 10:48 AM Response to Reply #10 |

| 11. The report didn't say we have to cut SS. |

| Printer Friendly | Permalink | | Top |

| doc03

|

Thu Jan-27-11 11:03 AM Response to Reply #11 |

| 13. No it didn't say we have to cut SS or raise taxes either.. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jan-27-11 11:07 AM Response to Reply #13 |

| 14. Are there any lobbying organizations for protecting SS. |

| Printer Friendly | Permalink | | Top |

| doc03

|

Thu Jan-27-11 11:13 AM Response to Reply #14 |

| 16. I think anymore the AARP is more interested in selling |

| Printer Friendly | Permalink | | Top |

| doc03

|

Thu Jan-27-11 11:11 AM Response to Reply #11 |

| 15. According to another post the report does take into account |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jan-27-11 11:20 AM Response to Reply #15 |

| 18. Agreed. |

| Printer Friendly | Permalink | | Top |

| ChoppinBroccoli

|

Thu Jan-27-11 11:03 AM Response to Original message |

| 12. Another Victory For Tax Cuts!!! |

| Printer Friendly | Permalink | | Top |

| Name removed

|

Thu Jan-27-11 11:20 AM Response to Original message |

| 17. Deleted message |

| lumberjack_jeff

|

Thu Jan-27-11 11:29 AM Response to Original message |

| 19. The reason there's a trust fund at all, is because boomers agreed to a big tax hike in 1983 |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jan-27-11 11:35 AM Response to Reply #19 |

| 20. "The fact that this trust fund would eventually be depleted was the intent." |

| Printer Friendly | Permalink | | Top |

| DaveinJapan

|

Thu Jan-27-11 08:26 PM Response to Original message |

| 31. Thanks to all. Lots of valuable info here, much appreciated! nt |

| Printer Friendly | Permalink | | Top |

| DU

AdBot (1000+ posts) |

Tue Apr 30th 2024, 11:06 PM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » General Discussion |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC