We've "streamlined" the regulatory process for nuclear power, and

we've provided guarantees that any delays related to regulatory changes will be paid for by the government, and

we've capped liability for a Chernobyl scale accident, and

we've given the utilities in the states where they are building the plants the authority to charge consumers for the costs even if electricity is never delivered so,

you might wonder WHY the investment community still sees a risk.

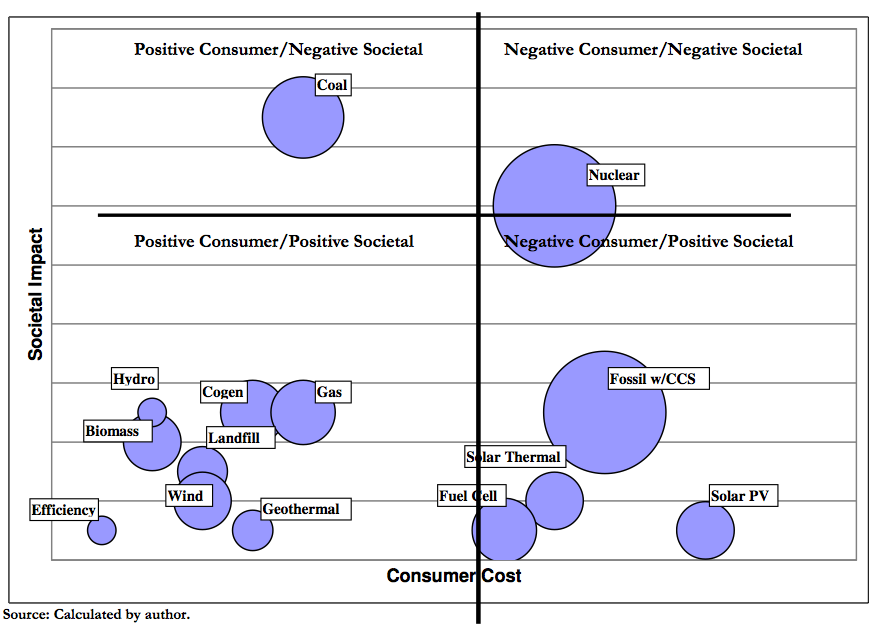

The Citigroup analysis for Europe (below) shows the long term viability problem faced by these huge projects. The charts below that highlight the fundamentals at work.

Citigroup 2008 impact of renewables and energy efficiency

What the market should not take for granted

GDP impact on demand and load factors

Consensus view is that electricity demand in the wide European region will grow by 1.5% p.a. over the next couple of decades. This is a view shared by UCTE in its latest System Adequacy Report. Although it is virtually impossible to produce irrefutable electricity demand forecast we are tempted to argue that the risks are on the downside since:

1. During the boom years of 2003-07, when GDP growth was strong and infrastructure investment high on the back of very liquid debt markets and due to the convergence of the new EU joiners, electricity consumption grew by 2.1% p.a.

2. Energy efficiency is likely to become a bigger driver as technology advances and as awareness rises. It is important to highlight that such measures also fall under the Climate Change agenda of governments, which has been one of the driving forces behind the renaissance of new nuclear.

As a result, we would expect electricity demand growth to be in the 0-1% range for at least the next 5 years, before returning to more normal pace of 1.5-2%. We therefore see scope for an extra 346TWh of electricity that needs to be covered by 2020 vs. 2008 levels.

Should EU countries go half way towards meeting their renewables target of 20% by 2020 that would be an extra ca. 440TWh. Even if EU went only half way, which by all means is a very conservative estimate, that would still be ca.220TWh of additional generation. Under its conservative �scenario A� forecast, UCTE expects 28GW of net new fossil fuel capacity to be constructed by 2020. On an average load factor of 45% for those plants that�s an extra 110TWh.

Therefore under very conservative assumptions on renewables, we can reliably expect an extra 330TWh of electricity to be generated by 2020, leaving a shortfall of 16TWh to be made up by either energy efficiency or new nuclear.

There are currently 10GW of nuclear capacity under construction/development, including the UK proposed plants that should be on operation by 2020. If we assume that energy efficiency will not contribute, that would imply a load factor for the plants of 18%. Looking at the entire available nuclear fleet that would imply a load factor of just 76%. We do believe though that steps towards energy efficiency will also be taken, thus the impact on load factors could be larger.

Under a scenario of the renewables target being fully delivered then the load factor for nuclear would fall to 56%.

(Bold in original)

Citigroup Global Markets European Nuclear Generation 2 December 2008