| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » Topic Forums » Environment/Energy |

|

| OKIsItJustMe

|

Wed May-06-09 04:56 PM Original message |

| The Battle Over Bolivia�s Lithium and the Future of Energy |

|

http://towardfreedom.com/home/content/view/1582/1/

The Battle Over Bolivia�s Lithium and the Future of EnergyWritten by April HowardWednesday, 06 May 2009 In the brine under a crust of blindingly white salt in Uyuni, Bolivia, lies nearly 50 percent of the world�s lithium reserves. Best known as a tourist attraction, the Salar is gaining fame as batteries made with this scarce element catch the attention of governments and auto-makers world wide. While on the campaign trail, President Obama promised that by 2015, there would be 1 million plug-in hybrids and electric vehicles on US roads, and, once in office, he allocated billions of economic stimulus package dollars toward battery technology and manufacturing. In Bolivia, leftist president Evo Morales wants a state-run lithium refining and battery manufacturing industry to generate funds for health, education and poverty alleviation programs in South America�s most poverty stricken country. As environmental and nationalist rhetoric promise big changes and bigger money for manufacturers and governments, questions still remain about the environmental effects lithium refining could have on Bolivia�s farming and tourist industry, and the viability of lithium batteries as an energy solution for the auto industry. A Superlative ElementLithium is the lightest known metal. At half the density of water, pure lithium has the disconcerting weight of a chunk of pine wood when held in the hand. You can cut it with a knife, but its white metallic luster tarnishes to an ashy charcoal almost immediately upon contact with oxygen. It floats in oil, burns with a bright crimson flame, and ignites in water. Modern society has used lithium in a variety of ways, ranging from mood stabilizing drugs, to the creation of the first human-made nuclear reaction. It is also used in glass, ceramics, light metal for aircrafts and, most importantly, batteries.� |

| Printer Friendly | Permalink | | Top |

| madrchsod

|

Wed May-06-09 05:35 PM Response to Original message |

| 1. china and tibet have the other large known lithium deposits |

|

Edited on Wed May-06-09 05:35 PM by madrchsod

there`s other ways to extract lithium but it is very expensive

|

| Printer Friendly | Permalink | | Top |

| kristopher

|

Wed May-06-09 10:55 PM Response to Original message |

| 2. The OP is based on an article that is a proved attempt at market manipulation. |

|

Edited on Wed May-06-09 10:57 PM by kristopher

It is regurgitating false information from a source that is trying to discredit lithium batteries in order to gain a market for zinc air batteries in the automotive industry. The quantity of lithium is from the bogus "report" as is the attempt to create an the appearance of opposition by environmental groups. Note that the article sources only this bogus report from "Meridian Research International" (it has even used the photos provided in the "report") and two NYT articles.

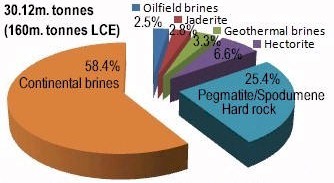

There are a couple of good points raised, such as the exploitation of a developing country's resources by corporations, but the basic story line is a great example of the gullibility so prevalent in journalism. - K. An independent assessment: Total Global Resources & Reserves of Lithium - At present noted Geologist Kieth Evans estimates total global resources and reserves of Li at 30,120,000 tonnes (160,000,000 tonnes Li carbonate equivalent). The following chart shows the estimated break down according to source types:  This break down will change over time as new entrants develop hectorite clay and oilfield brines Figure 1: Source; Notes taken by attendee to Jan./09 talk by Geologist Keith Evans Throughout noted Geologist Keith Evans' 40+ year career in the lithium industry he has made it his responsibility to monitor industry developments particularly in respect of new resources and he has continued as a consultant in a number of industrial minerals. The above is a snip of a longer piece specifically doing a market analysis on lithium for the auto industry at http://www.marketoracle.co.uk/Article9722.html "Geologist Keith Evans" has responded very specifically to the attempt at market manipulation here. Note the degree of misinformation in the article that underpins the OP: http://www.worldlithium.com/AN_ABUNDANCE_OF_LITHIUM_-_Part_2.html AN ABUNDANCE OF LITHIUM - PART TWO R. Keith Evans July 2008 ABSTRACT Estimated global lithium reserves and resources are increased slightly from the earlier figure to 29.9 million tonnes Li. This revision is written in response to a recent report which is alarmist in its gross underestimate of resources and, in several respects, ludicrous. 1. INTRODUCTION When Tahil�s first report �The Trouble With Lithium� appeared in 2007 he estimated a resource total of 21.8 million tonnes of lithium of which he classified 6.8 million as reserves with 15.0 million in a reserve base. The source of some of the numbers is unknown and several were of his own creation. What quickly gained this writers attention was his statement that �only lithium from brine lakes will ever be used to manufacture batteries. Spodumene deposits can play no part in this� and �only the second of these (brine lakes) are economically and energetically (?) viable for batteries". As someone who had spent 40 years in the lithium business I felt a need to respond and did so using the National Research Council Report of 1976, of which I was one of the authors, company annual reports, press releases, personal contacts with producers and with several companies with aspirations to enter the field. The writers of the NRC report decided that its aim was to describe and tabulate tonnages of lithium that could reasonably be expected to be developed in an environment of rapidly expanding demand � for fusion energy and peak storage batteries at that time. Accordingly, we did not feel constrained by the strict definition of reserves favored by the USGS and Bureau of Mines. One of the report writers was on the staff of the USGS and one formerly so. Similarly, my March 2008 report took the broader view. The term reserves as defined by the USGS needs to be restricted to material that can be economically produced at the time of determination i.e. that it can be extracted with existing technology at a specific price � usually the prevailing market price. The problem with this definition is that prices change and technologies develop. When SQM commenced production in Chile it halved the, then, current price of lithium carbonate. This made virtually all other production uneconomic and, thus not reserves. This did not happen because SQM only had sufficient capacity to meet a portion of, then, total demand. Regarding technological advancement it was not until the problem of treating brines with a high magnesium/lithium ratio was resolved could the large brine deposits in China become viable. The technology of producing carbonate from spodumene is well understood and it is this writers opinion that should demand grow at anything approaching the demand scenario postulated by Tahil, spodumene sources will be reactivated or developed. It will probably need somewhat higher prices to justify the necessary investments but it should be noted that a significant percentage of Chinese chemical production is currently from spodumene. Regarding other categories of resources described in my earlier paper-hectorites, geothermal brines and oilfield brines, test work is current on the first two of these and cost estimates for production from the McDermitt Caldera by Western Lithium should be available in the very near future. In addition to the categories previously described, another type of ore has recently been discovered in Europe � a sodium lithium boron silicate hydroxide named jadarite. The occurrence is discussed briefly later but preliminary test work indicates that magnetic separation of the ore produces a high grade concentrate and that the concentrate can be readily converted into lithium carbonate and boric acid. Another issue needs clarification. The pegmatite tonnages quoted in my earlier paper, specifically those derived from the NRC report allowed for mining, beneficiation and processing losses through to the production of carbonate. For the remaining, generally moderate sized pegmatites, the in situ tonnages are given. Similarly for all the brines the tonnages are in situ ones as recoveries vary greatly. 2. PEGMATITES - Reserves & Resources Tahil reverses himself somewhat in his second report where he states that because of differing chemical compositions it is easier to produce battery grade carbonate from spodumene rather than from brine. Nevertheless, he ignores them in his production scenario. All except one. The smallest and the lowest grade listed by myself � the Osterbotten (Larritta) deposit in Finland. He references one pegmatite in China versus my reserve estimate of 750,000 tonnes for the country as a whole despite the fact that several sources are currently contributing to Chinese carbonate production to supplement production from brine and imported spodumene. Russia is also ignored and only two Canadian deposits are listed � one of which is dedicated to profitably producing concentrates of a sufficiently low iron content that they are directly usable in glasses, glass ceramics and ceramics. Excluding Tanco, other known, but almost certainly underexplored Canadian pegmatites, contain 150,000 tonnes Li. In Zaire he describes the Manono and Kitolo pegmatites as a speculative resource. Hardly. He quotes Kogel's statement which, if it refers only to pegmatites, is almost certainly correct as �dwarfing the currently known world reserves�. Tahil further states that the figure I quoted of 2.3 million tonnes Li �tells nothing of the quality, grade and feasibility of extracting it�. The tonnage was published in the NRC report as 520 million tonnes of ore grading 0.6% Li (a typical grade for most pegmatites). The panel reduced the tonnage, all open-pitable, by 75% to account for mining, beneficiation and processing losses to give a total of 2.34 million tonnes of recoverable lithium. Any project would have the potential of co-producing tin, columbite and tantalite. One final comment concerns Bikita in Zimbabwe where Tahil says lithium carbonate has never been produced from this source. Carbonate was in fact produced in both Italy and the United Kingdom from both petalite and spodumene-quartz intergrowth of comparable grade (about 4.2% Li20) and approximately one third of the US Government's stockpile requirement for isotope separation (in the form of lithium hydroxide) was met from Bikita lepidolite. Bikita did not produce unprocessed ore. Lepidolite and petalite graded about 4.2% which in both cases is almost pure mineral and Tahil�s comment that 30,000 tonnes of product is equivalent to 1,000 tonnes of carbonate is incorrect. The correct figure is approximately three times greater. As a final comment the ore in North Carolina normally grades 0.6% Li, definitely not the 70 ppm quoted by Tahil. 3. CONTINENTAL BRINES - Reserves and Resources Tahil introduced in his second report a number of brine deposits seemingly in order to dismiss them as potential sources. They are Searles Lake, California, the Great Salt Lake, Utah, the Bonneville Salt Flats, The Dead Sea and sea water. I did not include any of these on account of their low grades although the NRC report included a potential for 260,000 tonnes Li from the Great Salt Lake from a resource total of double this tonnage. In the introduction to his second report, Tahil states that I included deposits grading as low as 8 ppm Li. That is nonsense. Tahil�s earlier report on the destruction of the World Trade Center (2006) was subtitled �Inconvertible Proof that the World Trade Centre was destroyed by Underground Nuclear Explosions�. He acquired the reputation among many as a conspiracy theorist and this attitude seems to be apparent in his observation on reserves; brine reserves at the Salar de Atacama in particular. He considers any increase in reserves over time as suspicious and the "inconvertible truth" is what he unilaterally decides is an appropriate reserve figure. Salar de Hombre Muerto Tahil quotes two reserve estimates � one for 130,000 tonnes Li and, from Garrett, a process engineer, for 800,000 tonnes. Tahil says the latter figure "appears reasonable" based on the grade of the brine and the area of the salar. The latter tonnage figure is in fact more or less correct and is based on an extensive drilling program which determined average porosity and the lateral and vertical variation in brine grade. If it was so simple as looking at grade and area Tahil�s "reasonable figure� for the Salar de Atacama would be about 10.0 million tonnes Li based on the differences in average grade (about 3 times higher) and size (about 5 times greater). Interestingly, about a third of the reserve at Hombre Muerto are at a depth of between 40 and 70 metres - a depth that Tahil says is too great for brine to be present. Salar de Rincon Tahil is suspicious about the reserves of the Salar de Rincon. Admiralty Resources the Australian company intending to develop the resource published a range of estimates (1.03 to 1.86 million tonnes) and, inadvertently, I used the highest figure. Tahil�s main concern, though, is that the figures in the company�s final reserve report are much higher than earlier estimates. The reason of course is that the earlier estimate was made when only a small portion of the salar had been drilled and there was no site-specific porosity data. There is, I acknowledge, some concern about the role played by the reported cavities that significantly increased the overall porosity of the aquifer. Personally, I would have to know a lot more about their size and location but Tahil�s comment that �it is unlikely that the Salar de Rincon has higher lithium resources or reserves than the Salar de Hombre Muerto � is meaningless. The company�s earlier comments about a significant lithium inflow from surface and ground waters (they are, almost certainly very small) were dropped in the final report. Salar de Uyuni Tahil�s description of the Salar de Uyuni is substantially correct but it doesn�t contain over 40% of global lithium brine resources. All realistic estimates are based on the work of a joint Bolivian and French team published in 1981. The average grade is 0.035% Li and 0.72%K with an area approaching Atacama average grades in the southeast of the salar. It is probable that any production would commence in this area but the development of any realistic production scenario will have to await the completion of a feasibility study and the percentage of reserves that can be economically recovered will be dependent upon the prices of both lithium and potassium chloride. Salar de Atacama Following the discovery of high lithium and potassium values in the brines of the Salar de Atacama, Corfo, a Chilean government agency charged with the promotion of production, secured the mining claims covering all the salar's nucleus. In the mid 1970�s they entered into negotiation with the Foote Mineral Company and Sociedad Chilena de Litio (SCL) was formed in which Corfo held a 45% interest. A four year study commenced in 1975 and the National Research Council (reported in Evans (1978)) quoted SCL�s reserve estimate of 4.29 million tonnes Li. Most of the exploratory work by SCL was concentrated in an area to the south of the salar and the reserves were split into two categories - 1.29 million tonnes in the area of detailed evaluation and 3.0 million tonnes inferred from geological evidence where the sampling was more widely spaced - a total of 4.29 million tonnes lithium. This was the first reserve estimate for the salar's nucleus. Tahils figure of 2.2 million tonnes in Figure 3 of his recent report is wrong. He misread the tonnages given in the NRC report. All reserve calculations in the early evaluations were in respect of the top 40 metres (not 60 metres). His second column figure of reputed USGS origin of 3.0 million tonnes has no rational basis. At the end of the SCL evaluation, Corfo allocated the company an area that was estimated to contain 600,000 tonnes Li (in my earlier report I erroniously stated that the area contained 500,000 tonnes) and in 1983 Corfo decided to invite bids to develop most of the remainder of the salar's nucleus (up to 790km2) and Amax and Molymet emerged as the successful bidders. Their proposed target was a project producing 500,000 tonnes/year of potassium chloride, 240,000 tonnes of potassium sulfate, 25,000 tonnes of boric acid and, initially, 2,800 tonnes of lithium increasing at approximately 7% per annum. On winning the bid Sociedad Minera Salar de Atacama (Minsal) was formed, in which Corfo was a 25% participant. Minsal�s evaluation programme extended over a period of about two and a half years but an ore reserve estimate was completed fairly early in the program based on a large number of core holes, near-surface sampling and geophysical work. The reserves were formerly approved by Corfo (and subsequently by consultants to the International Finance Corporation). The reserve estimate was for 24.5 million tonnes of potassium and 1.67 million tonnes of lithium at an average grade of 0.14% Li with lithium concentrations ranging from 0.09% to 0.30%. The reserves were calculated to a depth of 40 metres-the total depth of the vast majority of the cored holes and porosity data was obtained from 4, 500 core samples, not from one hole drilled by an oil company as stated by Tahil. When Amax decided not to proceed with the project it was acquired by Soquimich (SQM) and in renegotiating the agreement with Corfo a further small group of claims were added to the original 790 km2. These claims had been separately evaluated by Minsal for rapid development in a joint venture to produce potassium nitrate. This project did not materialize so the additional tonnages of potassium and lithium were added to the SQM claims. The additional tonnages of high grade brine increased the lithium tonnage and the average grade of the SQM block to 0.18% Li. The next reserve estimate emerged in 2007 when, after 10 years of operational experience, extensive additional drilling below 40 metres and detailed monitoring of a large number of observation boreholes, SQM announced that proved and probable reserves for lithium had increased to 3.4 million tonnes. In 2008 SQM stated that as a result of additional deeper and intensive drilling the current reserve totals 77.2 million tonnes of K and 6.0 million tonnes Li adding that all information gathered by SQM to date is substantially more reliable than information gathered through indirect methodologies such as surface geophysics more than 30 years ago. In the preparation of my earlier report I thought it appropriate to estimate a lithium tonnage for the Salar de Atacama as a whole. This is the sum of the Chemetall claims, the SQM claims, the buffer zones between them and a portion of the area to the north of the nucleus (the total Atacama brine covers 3,000km2) where lithium values remain high � higher than at the Bolivian and Argentinian salars. Proof of good grades in the sediments north of the salar's nucleus is the fact that a Chilean company is proposing a 200,000 tpa potash project there. As potash and lithium concentrate together this is indicative that lithium grades will be relatively high. The estimate in my earlier report was 6.9 million tonnes for the whole of the salar area but my estimate for the Chemetall area, so I have been advised, was 100,000 tonnes too low so the total should be 7.0 million tonnes Li. What Tahil has written about production from the salar, the world�s leading resource for lithium, is totally nonsensical. When Foote Mineral Company had a choice of claims they did not choose the area of highest lithium grades. Their choice was dictated by the need for an overall brine chemistry from two separate brine types that was appropriate for the lithium extraction technology they proposed. Their agreement did not allow for potash recovery (this changed later with a change in the Mining Law) so their only concern was lithium recovery and lithium feed grades at the operation approximate to the average for the salar�s nucleus. Minsal�s proposal was to take only a relatively small proportion of its feed from the area of highest potassium and lithium concentrations as the company proposed a single pond system which would allow the production of both potassium chloride and potassium sulphate. This required brine from closer to the centre of the salar�s nucleus with a higher sulphate content. SQM, however, decided to develop two pond/plant operations with potassium chloride and lithium from a southern location and potassium sulphate (and, later possibly, lithium) from a more northerly location. Normally, given a choice any mining company will mine the richest part of an orebody first for obvious reasons. This generally applies to any orebody, any mineral anywhere. Foote�s decision was an exception for the reason given. Naturally grades will decline with time necessitating the progressive increase in the size of the solar ponds but it is clear that even brine at the lowest lithium concentration encountered in the salar�s nucleus (0.09% Li) can be classified as ore grade when it is compared with the salars at Hombre Muerto (0.062%) and Rincon (0.033%). All Tahil�s comments about the legal status of the mining claims at the Salar de Atacama are totally incorrect. Both companies have leases and agreements with the Government (Corfo) and there are no depth limits on the claims. 4. OTHER POTENTIAL SOURCES Tahil seems to accept that oilfield brines and geothermal brines could have some potential. Whether any work on the former is being undertaken is unknown but Simbol Mining is now fully funded and laboratory work has commenced on the probable geothermal brine feed. Concerning hectorites, Western Uranium has now spun off its lithium interest into a separate company and test work is said to be encouraging. Recently RTZ announced the discovery of a potential major source of lithium and boron. Located near Belgrade in Serbia a deposit rich in a new mineral species named jadarite covers an area of nearly 5 square kilometers. The jadarite occurs at 3 horizons each averaging 14 metres in thickness. The current target is within the lowest zone containing between 80 and 100 million tonnes grading about 2% Li20 � about 850,000 tonnes Li(together with approximately 13.0 million tonnes B203). 5. POLITICAL & ENVIRONMENTAL CONSIDERATIONS Other comments by Tahil concerning the fact that � activists in Argentina are in a state of war against the mining invasion� and the reactivation of the US Fourth Fleet are not worthy of a response. His concern for the environment is commendable but if and when Uyuni is developed we would be looking at a project with a plant area covering about a square kilometer and solar ponds covering a few tens of km2 either on or adjacent to the salar. These at a salar covering 9,000km2! In Chile, his other area of concern, the companies are in full compliance of the stringent environmental laws backed by a vigorous environmental monitoring system. 6. RESERVE & RESOURCE SUMMARY Reserves and resources in my earlier report totaled 28.4 million tonnes Li. This figure is now slightly revised as seen below - I have reduced the Salar de Rincon tonnage by 0.46 million (a correction) but added back 0.3 million which is a very preliminary estimate for the Salar de Olaroz in Argentina being evaluated by Orocobre, an Australian company. For the sake of consistency I have included the total resource tonnage for the Salton Sea geothermal area and, finally, added in a tentative tonnage for the Jadarite project in Serbia. 7. SUPPLY & DEMAND My first report did not address the issue of supply and demand as it was beyond its scope. Demand projections vary greatly and I lack information on the timing of increasing production in China to have a realistic estimate of supply. The demand scenario postulated by Tahil is, though, an extreme one. He envisages the wholesale abandonment of the existing motor vehicle fleet and assumes that a very high percentage of all new vehicles will be Volt-sized. This ignores the fact that most older vehicles will continue to run on gasoline or biofuels and others will be powered by other battery systems, natural gas and possibly hydrogen, fuel cells and capacitors. In late 2007 in a presentation to European investors, SQM estimated that by 2015 ten per cent of new cars (5 million vehicles/year) would be powered by lithium-ion batteries rising to 20% by 2020 increasing annual demand for lithium carbonate from 85,000 tonnes in 2007 to 160,000 tonnes in 2015. Other estimates of demand vary greatly. With the recent increase in gasoline prices there is ever increasing pressure to produce lithium-ion batteries for vehicles but the lead time is dictated by technology not the availability of lithium. The Chinese are seemingly expanding capacity but only SQM among the South American producers is currently undergoing expansion despite the large reserves available at both the Chemetall and FMC operations. The pegmatite deposits in Canada (except Tanco) for example, have been sitting there for years awaiting a market and even with their existing reserves could be jointly producing about 50,000 tonnes/year for a 20 year period and the previously abandoned North Carolina operations could probably be reactivated. The necessary technology is well known and the price necessary to make production economically viable is readily determined. Numerous China producers and two companies, one in Australia and one in Europe believe that production from pegmatites is viable at current prices despite the relative low grades of their two respective deposits. A rise from the current levels is probably necessary but the cost of carbonate in batteries is a very small percentage of the battery cost. Where hectorites, geothermal brines, oil field brines and jadarite stand on the cost ladder remains to be determined. |

| Printer Friendly | Permalink | | Top |

| OKIsItJustMe

|

Thu May-07-09 02:26 PM Response to Reply #2 |

| 3. According to the USGS |

|

http://minerals.usgs.gov/minerals/pubs/commodity/lithium/mcs-2009-lithi.pdf

� (5,400,000 in Bolivia.)World Resources: The identified lithium resources total 760,000 tons in the United States and more than 13 million tons in other countries. � |

| Printer Friendly | Permalink | | Top |

| DU

AdBot (1000+ posts) |

Wed May 01st 2024, 04:01 PM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » Topic Forums » Environment/Energy |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC