General Discussion

Related: Editorials & Other Articles, Issue Forums, Alliance Forums, Region ForumsIf you do not have 20% as a downpayment for buying a house you should rent. Period.

If we had had that rule - I would have had to purchase a house later than I did - but it wouldn't been so inflated in value and I would have had more equity in it by now.

My misery aside - I think a person/family needs to put real skin in the game, before buying a house. It keeps speculators out and the market a bit more stable.

We should not relax the rules for downpayment.

what do you think?

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

Marrah_G

(28,581 posts)I don't necessarily disagree with you, but at the same time, prices would need to come down and wages would need to go up or else there will end up being alot of abandoned and bank owned homes.

Agschmid

(28,749 posts)I could not agree more, I will never own a home if that was really the rule.

Marrah_G

(28,581 posts)it sucks!

Agschmid

(28,749 posts)For 6 mos to a year (I am 28 right now) and save as much as I can, then roll that and my 401k into a down payment for a house...

So scary!

Good luck finding a place!

SharonAnn

(13,771 posts)However, young families with children are between a rock and a hard place, sometimes. Limited rentals available for families with children, high cost for those rentals, and so less money for down payment. Maybe 10% is more realistic.

Orrex

(63,172 posts)Your system ensures that lower- and middle- income families will never own anything, but if they work hard enough for their entire lives, they might scrape together enough money to buy a cardboard coffin and a pauper's grave.

Bravo!

clarice

(5,504 posts)

Warpy

(111,163 posts)to live on plus manage to save a little.

Our economy is brutal after 40 years of wage depression as a basic policy issue.

Haven't you noticed?

clarice

(5,504 posts)

Gin

(7,212 posts)Your system ensures that lower- and middle- income families will never own anything, but if they work hard enough for their entire lives, they might scrape together enough money to buy a cardboard coffin and a pauper's grave.

Bravo!

>>>>> This part <<<<<< This DU Member is not permitted to post replies to this thread.

Common Sense Party

(14,139 posts)dkf

(37,305 posts)As long as people accept the downside with the upside then it's their choice. But you can't expect you will either increase your wealth or get to stay in your house regardless of ability to pay.

If you take the risk you must accept the consequences.

Orrex

(63,172 posts)Forgive me, but no kidding. I submit that no one is more acutely aware of the consequences than the person who has suffered through foreclosure.

20% is also a fatal threshold for the majority of the country, I should think. It's entirely reasonable that a family can afford $700 for a monthly mortgage on an $80K home but can't afford to save up $16K while paying $640 for monthly rent in advance of the home purchase.

Also, 20% doesn't mean the same thing in all contexts. Our first home was $53K, and we offered to make a 10% downpayment. After some quick calculation, we were informed that this would amount to $12K, rather than the $5300 we were expecting.

Rather than setting some arbitrary and unattainable number, why not be up front about it and tell people that they simply don't deserve to own property?

dkf

(37,305 posts)Improved chance that you will get the mortgage—The first and biggest reason to come up with 20 percent down is that in today’s new market, many banks won’t give you a mortgage unless you come up with at least that much. The loan programs that once existed for 10, 5, and 0 percent down are not just not available.

Skin in the game—Twenty percent has been the norm forever. It really serves to ensure that the homebuyer has “skin in the game” and is financially viable for the homeownership responsibility.

Smaller monthly mortgage payment—More money down means you borrow less, which means you will have a smaller mortgage, which means you will have a smaller, more affordable mortgage payment.

Lower interest rate—The interest charged on a loan with 20 percent down is often lower than the interest on a loan with less money down. Your lower interest rate will save you thousands if not tens of thousands of dollars over the life of the loan.

No private mortgage insurance (PMI)—Putting 20 percent down allows you to avoid private mortgage insurance. Also called lender’s mortgage insurance, PMI is extra insurance that lenders require from most homebuyers who obtain loans in which the down payment is less than 20 percent of the sales price or appraised value. Many lenders will even add a percentage that is like an insurance policy onto the mortgage interest rate.

Instant equity building—A significant down payment builds instant equity in your home. A 20 percent down payment immediately puts equity into a property when you purchase it. That down payment safeguards you if the market turns downward temporarily.

Great saving skills—Saving for a full 20 percent down is a great way to establish practical and healthy saving practices. If you have saved up for 20 percent down, you have probably learned how to manage your money wisely. That skill is going to come in very handy because the money outflow doesn’t stop once the seller hands over the keys to the front door!

http://m.trulia.com/blog/michaelcorbett/2012/04/seven_reasons_to_put_20_percent_down#

Orrex

(63,172 posts)Here's the bottom line: people must prove that they're better at managing money than the banks that lend it.

Again, if we're going to adopt a generally unattainable standard, then we should be honest about it and declare outright that the intention is to lock people into their serf class with no ability to own anything of substance.

srican69

(1,426 posts)This deserves a bookmark.

we can do it

(12,173 posts)This is the banks rule. It excludes too many lower income people who are paying the mortgage the "investor" has on their rental. There were a huge amount of "investor" owned properties that were just walked away from when the home prices dropped. These same assholes are now inflating rent on properties they picked up dirt cheap. Working people deserve a chance to own.

geek tragedy

(68,868 posts)If you have only 10%, different story.

DotGone

(182 posts)For the buyer, a down payment means more of their money is in an asset that may not be liquid. Sure you have equity but 60K in cash vs 60K in a house you can't sell? I'd take the former. Or a worst case scenario where your equity position is worth more than the house but you're still stuck with a mortgage. You walk away, you lose your down payment amount. A down payment is a safety mechanism for the bank though. Banks want the down payment so they're not stuck with the full bill when you walk away.

BlueStreak

(8,377 posts)There are lots of good properties for rent at every level of the housing market. The whole concept is "get ahead by buying a home" is mostly nostalgia that no longer is good advice. People should not expect their house to appreciate. If you are 99% sure you will live in that house for at least 5 years, then ownership is a reasonable proposition. If it is unlikely you will stay there 5 years, then rent. Your chances of coming out ahead in this deal are very low.

If you expect to be in the place for 5 years, but can't afford the 20%, then look at a more modest property where you can afford the 20%. Then spend the next 5 years accumulating some savings so that you will have the option to move up to a nicer property when YOU can control the timing.

All these "reality teevee" shows with auctions, house flipping, home makeovers are bogus. The only people who consistently make money in housing are those who:

1) accumulate good properties at a low price and rent them.

2) people who are willing and able to do a lot of sweat equity to fix up a property that has big problems.

Renting is not a bad thing. In many cases, it is the smart decision.

Time to end the mortgage exemption that has created a false economy in housing.

Where'd you get those prices? The 1980's?

Where'd you get those prices? The 1980's?

Orrex

(63,172 posts)Go on with your bad self.

NutmegYankee

(16,199 posts)Your prices were just not reflective of the markets, particularly on the coasts.

cyberswede

(26,117 posts)The fact that houses in many markets (if not most) cost significantly more than his example only makes his point more valid.

How many young people can come up with $50,000 down for a $250,000 home?

Orrex

(63,172 posts)It wasn't a personal attack, any more than your observation was intended to be. Perhaps I misread your tone, and if so then I apologize.

As others have noted, the prices that I mentioned are applicable in a number of places. $80K would buy a very nice home in my area, for instance.

truegrit44

(332 posts)You can rent a really decent house here in MO for less than $600 per month and buy a real decent place for $80,000.

kcr

(15,315 posts)Depends on the part of the country you live in.

wercal

(1,370 posts)You do your own self a disservice if you don't have a good down payment.

Especially in today's market, where the values of houses are static...if you're looking to build wealth, you'll get a better return in a money market than a house right now. Especially if you're being nickel and dime for PMI (usually required for equity below 20%)

And along with home ownership comes risk. Stuff breaks - you fix it. I've replaced a/c units, a sewage pump, a few hot water heaters, a roof, and repainted over my years of home ownership....so its not exactly a gold mine when you own sometimes.

And you are 'tied down'. I've turned down an opportunity to move to a better position in my company, because the house ties me down. I can't liquidate it in an instant. Imagine how tied down you would be with no equity - the inspections and half the realty fee would have to be cash from your pocket...and if you don't have it, you're a house prisoner. Same goes if the value drops.

I think its up to the lender to set their own threshold...but as a borrower, I'm glad I had a good down payment, or I would really be trapped. And, I recommend a large down payment to others.

geek tragedy

(68,868 posts)be with a smaller downpayment?

wercal

(1,370 posts)You've heard of the term 'underwater', right?

Let's say I bought a $100k house with a 5% down payment. A year later I lose my job and try to sell it - and discover the house has lost 10% of its value, and is only worth $90k now.

So, I owe around $94k (1 grand of equity might get paid in year one)...but I can only get $90k for it. Add $3,150 for a 3.5% realty fee, and half of inspection costs (add another $350)...and I have to come up with $7,500 just to sell my house. Which would be mighty hard if I were unemployed. So, I'm stuck...I can't make payments, ruin my credit (inflating any interest costs I will pay on a future house purchase), and eventually it gets foreclosed on.

What if I had put $20k down? My cost to pay of the mortgage is now $82,500...meaning I am able to sell the house, pay all associated fees, prevent a life altering foreclosure, and walk away with $7,500 to pay month to month rent somewhere in a different city, where you can find a new job.

See the difference? One option causes a whole lot of stress in your life, and restricts your choices...and ruins your credit and affects your future. The other gives you freedom to act.

geek tragedy

(68,868 posts)Obviously, if you're going to move in 2-3 years renting is the better option anyways.

And not all real estate markets are static. We put 10% down on our place in 2010 (90%) LTV. We're now sitting at 57% LTV after we refi'd, and our carrying costs are about 2/3 of what it would cost to rent our place.

Plus tax break.

wercal

(1,370 posts)...and would just rather hold onto it, than put into a downpayent. There are upsides and downsides to that, but quite frankly most people on this thread who don't like a downpayment are giving reasons that deal with a person's inability to accumulate the money in the first place. They don't have it in hand, and their complaint is that they never will. For people in that situation, I strongly recommend Renting.

But back to the situation where a borrower has the $20k, but only wants to put $5k down and hold onto the other $15k. First of all, the borrower (and their spouse) have to be disciplined enough to not dip into that money to buy a new boat, etc. And, if they are, it becomes a numbers game. What interest do you pay on that as borrowed money vs what it earns in savings? And, can you get a lower rate with a larger down payment? Another factor is PMI...an expense that disappears when you get to 20% equity.

I think mortgages are at 3% now, and savings accounts are 1-2%...so unless I'm missing something, you do lose money by keeping it out of the downpayment, in today's market. And, you pay a little for PMI. But, I can understand the sentiment of not tying the money up....just know you'll lose a little bit of its value every year. I actually concur in a sense, that I think it is risky to deliberately amass equity beyond 20%, any faster than the amortization calls for. I'm sure BOA has an express lane for foreclosure on properties with over 60% equity...they can file after one late payment and steal your equity right away from you. So I do agree that a seperate savings account, for a balloon payment at the end, is better than using the mortgage as a depository for savings.

As far as values go, if yours has risen so much in the last 3 years, I would say you live in a very hot market. My valuation from the tax appraiser has stayed the same for 4 years now...and I don't live in an area that was terribly affected by the housing crisis. But, as you know, many people live in houses that have lost 20-25% of their value - and they are trapped beyond belief. They would have done themselves a favor by either making a large down payment, or at least having it 'on hand'....but 99% of the people who don't want to make a large down payment are of that opinion because they absolutely can't.

BTW, I still think the housing market hasn't hit bottom yet (at least in some areas). As an example, I bought a house for $93,500 in 1994...and sold it for $172,000 in 2006. However, if the house value were to have been tied to an average inflation of 3%, it should have been worth $133k at that time. So it was over-valued. Extending inflation to 2013, it should be worth $163k....so inflation still hasn't caught up, and the house still has 5-6% of its value to lose. So, I still don't think its a great time to buy (in most places).

geek tragedy

(68,868 posts)each and every situation is idiosyncratic.

Tax benefit, for example, means a lot more to a person buying a $500K property than one buying a $150K property, especially given the respective likely income tax brackets.

Not to mention employment/income stability (how important are reserves), prospect of moving, other forms of debt to pay down, market factors, etc.

Our market (Brooklyn) is white hot--lots of pent up demand being released, with tight, tight inventory (98% reduction in new construction inventory from Q42012 to Q12013). Classic moment back when we bought of "will we regret it for the rest of our lives if we don't buy now?"

Answer would have been yes.

But, it was tough enough coming up with over $60K in down payment and closing costs just for 10% down. 20% would have meant six figures out of pocket. Who has that kind of money?

wercal

(1,370 posts)I live in the mid-west, in a $170k home.

I could not fathom buying a half million dollar home.

And for me the tax benefit is negligible...I itemized around $1k above my standard deduction.

For this reason (at least in my area) I think renting should be a serious consideration. I actually gave this advice to a friend a few weeks ago.

IMHO, Brooklyn benfits from geography. Its not like the city is going to sprawl and get bigger - so even very old houses hold their value. In California, the same is accomplished by limiting building permits each year. In the mid-west, where I live, the city boundaries can always expand. So, its a 'flight' out of the older parts of the city, and neighborhoods decline and become so dangerous, that nobody wants to live there (think parts of Chicago and Detroit). Anyway, no matter how bad the housing market gets in a place like Brooklyn, it seems that it will ALWAYS bounce back. So I could see a bank lowering the down payment threshold on a house in Brooklyn, without thinking twice....and your own risk of a dramatic loss of property value is almost nihl.

Contrast that to Las Vegas, where there are endless subdivisions of empty houses - there is practically no value in these houses.

So, I approached it from a midwestern perspective, and I certainly didn't consider how different a New York buyer might view things.

I think there is an adage about all real estate being local, or something like that.

geek tragedy

(68,868 posts)When the market is hot, you're talking 25-50% down in cash. Sometimes for just a floor plan.

That's the developers/sellers dictating things, not the banks.

The Great Recession only slowed down the gentrification wave.

For people in NYC in the federal 28% tax bracket, when combined with state and city taxes, the tax deduction is worth $400 for every $1000 deducted. So if they pay $1500 a month in interest, that winds up being $18,000 deducted from taxable income, or to put it another way $7200 of cash back in their pocket.

Real estate in sparesely populated places tends to be driven by cost of land and construction--in cities it gets driven by demand.

tridim

(45,358 posts)So, be careful. I guess.

At this point I'm not sure if I'll ever be able to pull the trigger on a home purchase again.

Orrex

(63,172 posts)The bank didn't steal your home--you made bad choices and didn't pull yourself up by your bootstraps, etc. etc. etc.

You have my sympathy re: the loss of your home. It's a nightmare that no one should have to endure, least of all because of the wrongful actions of others.

Agschmid

(28,749 posts)I'm not in disagreement but you are a bit feisty today... Although we all have those days...

sinkingfeeling

(51,438 posts)Wounded Bear

(58,603 posts)maybe I'll get back to you.

Bluenorthwest

(45,319 posts)payment would be less than the rent on the same fucking house and I don't see the logic in that. Why pay more in rent than you would to buy? To prove some point?

bowens43

(16,064 posts)sorry but that makes no sense. My son just bought a house with much less than 20% down, his mortgage is a LOT less then rent would be. It would make no sense for him to pay rent. Your rule would ensure that the vast majority of Americans would never own a home.

Lars39

(26,107 posts)

MAD Dave

(204 posts).....why 20% is not attainable for most people. The wage earners in North America have been screwed 18 ways to Tuesday by a series of spectacularly shitty governments hell bent on destroying the middle class.

An enforced 20% would put my family out of the homebuyers market for 10-ish years. I'd almost be 50.

Yeah that's fair and just! To boil it down, I feel like I have been screwed over royally by decisions made by my parents and grandparents generation.

Lars39

(26,107 posts)MAD Dave

(204 posts)....maybe 10% of an average house in our market. But until my wife is employed again, we're hand to mouth again.

On a positive note, I started a new job last week. Unionized, decent benefits and some upward mobility. Things may be getting better, I hope.

Lars39

(26,107 posts)

socialist_n_TN

(11,481 posts)That means that the CAPITALISTS are the ones who OWN the government. So you might as well blame the REAL bosses behind the façade of government.

Mopar151

(9,975 posts)And the cash outlay at closing is a good deal more than the down payment, especially if you are dealing with an FHA or similar "low down payment" loan.

reformist2

(9,841 posts)

ohheckyeah

(9,314 posts)We didn't have 20% down but we could more than afford our house payments and the house appraised for more than we paid for it. We've been in the house for 10 years now and our payment is a lot lower than anything we could rent that would even be close in size.

For many people the "real skin in the game" is the emotional attachment. Speculators for the most part can afford 20% down.

upaloopa

(11,417 posts)benefits for society and for the individuals involved.

Neighborhoods are more stable when most people in the neighborhood own their homes.

There are the tax advantages to deducting interest and taxes reducing your tax burden. There is the desire and ability to spend money on improvements which adds to the economy. I could go on but we set up VA and FHA loans because home ownership is good for the country as a whole.

Personally I got all my home loans as VA loans. I built up equity which I never could if I rented or had to pay 20% down which I never could have saved. It is my only chance at any kind of investment.

Renting makes money for landlords who have enough already to buy rental property.

Home ownership puts you in the game also. Rents would certainly go up due to the demand were renting could cost more than a mortgage.

supernova

(39,345 posts)for a mortage. That is increasingly hard ot come by. Most people have to change jobs every 3-4 years at the very least. The days are gone when you could get hired and expect to be there 10+ years longer. And forget about ever increasing paycheck to help save more over time or help the mortgage not seem like such a big bite.

Job churn is another thing that prevents people from saving.

Cleita

(75,480 posts)property I could call my own and as an investment. Not having the down payment always kept that privilege away from me. Some get lucky, but most of the lower third in income and wealth in this country never get good breaks to lift themselves up from that. So not having to make a down payment or at least not a large one for many became a path to home ownership. I think the big culprit here was the mortgage rate shenanigans. Mortgages should be a fixed rate and not adjustable rate and they shouldn't be in the double digits. A straight old fashioned mortgage like they used to be wouldn't have created the mortgage crisis we have today.

neverforget

(9,436 posts)

snappyturtle

(14,656 posts)if you look at amorization tables and plug in more down payment

it doesn't greatly affect the mortgage payment....at least when I

was contemplating on a fixed (yrs.) mortgage. That got me to

thinking since the down payment is coming out of savings that I

might be smart to with hold some of the dp for "rainy day' funds

like when the furnace poops out. You sound like my daughter who

unfortunately had her arm twisted to buy now before prices go even

higher and now she is stuck with a home that has lost a lot of value.

Of course, her property taxes have dropped and s-l-o-w-l-y property

values are inching back. This is in the Minneapolis area.

Yesterday I listened to a video of Richard Wolff's (I think...been watching

a lot of economists) but anyway, he said that we will see more foreclosures

this year than we have annually in the last few! In other words the

housing market is not recovering despite what we're hearing on the

news. Who do you believe?

As far as buying vs. renting? I think if one is very careful and does not

buy too much, buying far exceeds renting. I'm renting now for 15 mos.

First time in over 40 years for me and it stinks. I have nothing for

my payments investment wise. Rent is so high that in the two markets

I'm combing through I can buy cheaper/mo. than rent by far. SOoooo...

20% down, "Yes" but although I can buy outright, not looking at a

castle (ha!) I don't think I want too much skin into it. I guess I'm

hedging...horrors! Good luck on whatever you decide...do your homework!

Godhumor

(6,437 posts)Let us say a couple wants to buy a 200k house. Today they can lock in a rate of 4.5% but only have a 5% down payment. So they decide to wait until they have saved 20%. By the time they do so, the rate has gone up to 6%. How much do they save by putting up the bigger down payment? 3 bucks a month.

And they still have a 30 year mortgage, too.

Blue_In_AK

(46,436 posts)with zero down, which was a good thing because I didn't have any money to speak of, and my landlady had just been foreclosed on, forcing me into a buy situation (rental vacancy rate here at that time was about 1% and I had large dogs). This was a HUD foreclosure. Generally, though, I tend to agree with you that it's good to put some money down, probably not as much as 20%, though. That's a lot.

JVS

(61,935 posts)Loan amortization works in such a way that the borrower builds equity very slowly in the start and very quickly at the end. The problem from the lender's point of view is that since the collateral on a mortgage is the property itself, the borrower can always walk away from the debt if he/she doesn't mind losing the equity. Low down payments mean that equity stays low for a very long time and the buyer doesn't care about losing the equity for a longer time. Large down payments make it less tempting for the buyer to walk away from the debt because it exposes them to bigger loss from the beginning.

FarCenter

(19,429 posts)If the lender can't sell the house for enough to reclaim the unpaid balance on the mortgage after selling costs, the lender goes after the borrower for the "deficiency" and will seize other assets, garnish wages, etc. The borrower then either pays the deficiency or goes through bankruptcy.

Rider3

(919 posts)That you should go over the numbers, get to a figure you KNOW you will be able to pay, and lock-in. I didn't pay 20% when I purchased my home in 2000. Instead I put down $5,000. I was also told by the mortgage company that I qualified for more than I asked. However, I KNEW that I knew my finances better than the guy pushing the mortgage. I stayed within what I knew I could pay, and purchased the house. 13 years later, we're still there and haven't missed a payment. If I had listened to someone else, I probably would've been foreclosed upon. Buy what you can afford. Don't try to keep up with the Romneys.

geek tragedy

(68,868 posts)Very few first-time home buyers have the 20% to put down.

Most people buying a home for the 2nd or third time do have that downpayment.

Do the math.

a la izquierda

(11,791 posts)Some of us have student loans and great jobs that don't pay 6 figures. I will buy smart and my mortgage will be less than renting.

What a stupid post.

Kalidurga

(14,177 posts)It doesn't really save you all that much on your mortgage and for most people including me it would wipe out contingency money. Also even if you are buying a brand spanking new house there is always something that needs to be changed or something you would want changed. It's cheaper to pay the mortgage than to borrow the money to make those changes. If you are buying a fixer upper then a contingency fund is even more important because you never know when the furnace, water heater, electrical system, roof, or some other big ticket item is going to need to be replaced/repaired.

GitRDun

(1,846 posts)The smartest way to buy, regardless of % down payment is to make sure your loan payment will not exceed 25% to 30% of your monthly incoming cash flow. People generally will not default using this formula unless something really big happens.

Little Star

(17,055 posts)on my first house. Just had a great, caring real estate agent who worked with the sellers & bank to make it happen.

I never defaulted on a payment and never rented again and that was about 45 years ago.

Down payments don't make you a responsible person. You either are are you aren't. But even a responsible person can fall on hard times and that down payment won't help them one bit but it will help the mortgage company.

Down payments are safety nets for the banks, period.

Thems my two cents.

CK_John

(10,005 posts)

Mosby

(16,260 posts)I support the First Time FHA loan program where the buyer puts down 5 percent.

For the rest 20 percent is fine.

People forget that it wasn't just the banks that created the "housing bubble" it was dirty appraisers and dirty real estate agents that made sure the prices kept going up, and they are back to doing this after a short break. The big lenders are aware of this which is why they are now requiring second appraisals from approved appraisers.

I just talked to a new neighbor this morning in fact, the first appraiser (who works with the real estate agent/shark) came up with a 299K value but Wells Fargo said "hell no" and the guy hired his own appraiser who came up with 235K. Guess what he bought the house for.

BlueCheese

(2,522 posts)From a lender's point of view, the down payment is protection against the borrower defaulting if the house loses some of its value.

From the borrower's point of view, there's no direct advantage in paying a down payment. There may be indirect benefits, however, such as getting a lower interest rate and having less principal to pay down.

Yo_Mama

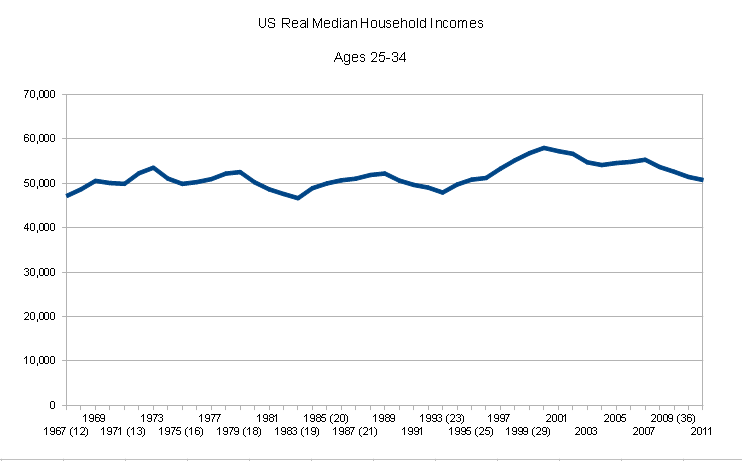

(8,303 posts)Even if you had a 10% downpayment requirement, it would prevent home prices from rising so disproportionately to average incomes.

For lenders, they make up the risk of default on high LTV loans by using private mortgage insurance or FHA. It is borrowers who wind up paying extra. This is a graph of US real median household incomes for the 25-34 age bracket:

This is a graph of purchase prices:

Something's got to give. I'd go with a 5% downpayment requirement so as not crash the market, but constantly lower downpayment requirements has fueled speculation and greatly inflated home prices past where they should be, historically speaking.

Orrex

(63,172 posts)Warpy

(111,163 posts)I was fortunate that a decent little fixer in a slum didn't exceed my savings. Even then, I held 5% back and only put 15% down. That meant the stupid mortgage insurance, but the cash cushion in case of disaster was even more important than a slightly bigger bite in the monthly payment.

I bought as a hedge against rising rents. 2 years later, rents were close to my monthly payment.

Since a buyer is going to pay 300% of whatever is on the mortgage note, usually the highest down payment s/he can manage is best. I don't think anyone these days will write a mortgage unless there is a down payment of some size. Housing prices have been flat or decreasing for too long for any more of those nothing down liar loans to be written and lenders want the buyer to take the hit on home equity, not be under water on the loan.

That 20% is arbitrary. It could just as easily be 10%. It's just a number bankers threw out 70 years ago. It is not written in stone and passed down through the ages. Today, it's an unrealistic number and will be as long as Congress is full of cheap labor conservatives who won't raise wages.

JVS

(61,935 posts)In much of the rust belt a perfectly good house can be purchased for between $30K and $50K, and modest homes can be found for $20k or less. In those markets, saving up a 20% down payment is not so difficult. Buying with cash even becomes an option.

ohheckyeah

(9,314 posts)and the house was inflated in price that has nothing to do with putting down 20%. It's up to the to the home buyer to find a house that isn't inflated and to buy when they are financially stable and ready. If you want more equity add a bit to your payment every month.

20% down is way out of range for many people because of low salaries and the high cost of living. It's punitive for the low and middle economic classes.

question everything

(47,437 posts)The problem during the bubble was that many had NINJA loans: No Income, No Job, No Assets - verifiable.

Many years ago, rule of thumb was to purchase a house at a cost of twice the yearly income.

Things have changed, of course, as price of houses rose faster than income.

But the main thing is for people to put something down. This way, they would not just walk away when they felt like it.

We purchased our house in 2002 with 10% down, 80% standard mortgage and 10% Home Equity Line of credit. We never used this line of credit except to pay it down, when their interest rate was high and they were playing funny accounting, we used a VISA loan to pay it off. That VISA loan, at 3.99% was paid off two years ago.

Yavin4

(35,421 posts)For the past 30+ years, we've been more concerned about getting access to credit to buy things instead of putting heat on our employers and politicians for better wages. Easier access to credit is probably the biggest driver of income inequality. Every dollar that you borrow, you have to pay it back with interest which is a direct wealth transfer.

That working class familiy needs higher wages to make that 20% down payment.

Gothmog

(144,934 posts)20% can be a large burden for most people. I do not think that you can get a mortgage now days with no money down. My first home was a 95% financed deal and the second was a 80% first 10% second and 10% down. My ex-wife and I made a great deal of money on that home. My last home was a 90% deal from a major builder and I just refinanced that home to get rid of PMI and to lower my interest rate.

Getting at least 20% equity does get rid of PMI and that is a good thing. I just refinanced my last home and got rid of PMI and lowered by interest rate by 262.5 basis points.

unapatriciated

(5,390 posts)The problem with the housing bubble was not because of how little or how much you put down. We bought a house in 2007 for 165k put 35k down, it is now worth 130k. We just lost more of our "real skin".

discntnt_irny_srcsm

(18,476 posts)...down-payment is meaningless. The only benefit to an increased DP is to make the monthly payments affordable.

If the payment is 25% of your monthly gross, it's a wise move to buy.

FarCenter

(19,429 posts)Suppose that the next day you sell the house. It will cost you about 8% in realtor fees, closing costs, etc. to sell (assuming no mortgage prepayment penalties, etc.).

If you find a buyer at the same $250K, the 8% is $20K. Therefore, you wind up with $30K left.

If you want to speculate in real estate, buy a REIT on margin.

we can do it

(12,173 posts)We only buy what we can easily afford on one of our salaries, so in case something happens we should be ok. We're now on house number 3. As long as people don't get carried away, there is no reason to restrict buying.

kestrel91316

(51,666 posts)rents for a 1 BR at around $1200 and 2BRs over $1400, it's virtually impossible for most people to save up enough for a down payment. Too few homes have 2 decent incomes anymore.

hobbit709

(41,694 posts)Our house was $500 down on a 25 year note.

Yo_Mama

(8,303 posts)I do think in one sense you are right - while instituting such a system now would cause a crash in home prices in most brackets in most places, if we had always had it you WOULD have a lot more equity now.

We jimmied the system for short term gain, but in the end the losers were all the people who tried to buy houses as homes, rather than speculation vehicles with living space.

Btw, for much of our history we did have higher downpayment requirements. 10% would be more the norm. Having a downpayment requirement preserves the ratio of home prices to incomes and prevents first time buyers from winding up underwater.

davidn3600

(6,342 posts)Banks and speculators are the ones that over-inflated the values and created artificial demand. This combined with unemployment and sinking wages created a perfect economic storm.

It's the banks and upper class that caused the conditions for a bubble to form.

srican69

(1,426 posts)Banks would have been forced to be selective with their lending practices.

The unfortunate thing is that it would also keep the responsible aspirers out of the market .. but it would only been a short while before they saved up for it ( remember the house prices also would have been lower)

NiteOwll

(191 posts)we would still be paying off someone else's mortgage by renting. Instead, we put only 5% down and have lived in our own home for over 10 years. We've never been late on a payment and always paid extra, even with job losses and layoffs. If we had to wait until we could put 20% down it never would have been possible. Besides the financial aspect, it's a better quality of life for us. Pets, gardens, space, home improvements, privacy, stability...things you don't always get renting.

Cosmocat

(14,559 posts)that would be REAL helpful is people not buying more home than they should in the first place.

Most of us and our friends bought our houses at the same time.

Lots of really nice, new, 3,000 square foot houses.

We went with a 1,700 foot house, then finished the basement.

We flipped from a 30 year to 15 year mortgage and are now 5 years from paying it off.

We had some tougher times over the last 5 years, but weathered it and are breaking back out of it.

HOPEFULLY that is the tough time, and we never missed a mortgage payment, had to tighten out belts a bit, do without some things, but overall still were comfortable.

Just no way people should max out coming out of the gates for a home.

Should absolutely live within your means and leave some breathing room.

0rganism

(23,930 posts)which is essentially what you're suggesting as a downpayment.

For a lot of middle-class and even upper-middle-class professionals, that kind of money is tied up in options or accounts with penalties for early withdrawal.

The home loan market's already gotten kind of rough. One of my co-workers is trying to buy a house now so he can relocate and he's paying through the nose just to have access to his money. Banks aren't as willing to sell mortgages based on eventual sale of your current house anymore.

Nice idea, but impractical for many people. You'd be reducing the buyer pool by a lot, maybe 40-50%.

srican69

(1,426 posts)When did average Joe live in 1/2 million dollar houses ..

most people lived in houses that cost far less until about a decade ago before everything went totally outawhack

geek tragedy

(68,868 posts)$500K gets you maybe a 2br apartment in Queens for that price.

srican69

(1,426 posts)geek tragedy

(68,868 posts)0rganism

(23,930 posts)You can say the market is "outawhack", overinflated, whatever, but that's where it is right now. So the problem is twofold. First, you're asking people to pony up an extravagant and not-easily-available amount of money for a downpayment. Then, as the buying market diminishes based on these arbitrary standards, you depress the housing prices significantly. Many people are counting on their homes appreciating over time for solvency in their later years, and if a homeowner is underwater on his/her mortgage, that presents problems of its own in terms of getting credit for other purchases.

You're not just requiring buyers to have a large amount of money on hand, you're setting every homeowner up for a huge loss in property value for housing they already own until the market restabilizes around what you consider a reasonable price point -- i.e., where a large segment of prospective buyers have the financial wherewithal to meet this new 20% minimum downpayment. The correction you're asking for could be quite severe.

wet.hen88

(64 posts)This seems to be a consensus. AND we are distrustful of banks and mortgagers as they are of us. Everything I read and hear from economists says bad time to plunge into that kind of debt. Unfortunately, prices and loans are so cheap, its tempting, Friend owns several nice apartment complexes...has 6 mos waiting list!

DesertFlower

(11,649 posts)of 10%. i put 20% so i wouldn't have to pay mortgage insurance. banked my salary for a whole year for the downpayment. the house was $164,000 with upgrades (pool, spa, etc). that was in '89. it was a slow housing market in phoenix back then. BTW. the house was in phoenix, but was still living in new york making a good salary.

tammywammy

(26,582 posts)I bought a house in 2007 with only $1500 to put in escrow...the mortgage plus escrow is cheaper than rent was. I had to pay PMI though. A couple of years ago I refied and knocked down my payment plus was able to get rid of PMI.

laundry_queen

(8,646 posts)and as someone who just bought a house with 5% down, I'll tell you why.

Where I live, rent is more expensive than a mortgage. By far. I've always owned a home - since I was 20 - mostly with my now-ex. I'm well-versed in home ownership. When he cheated and left me with 4 kids, I moved in with my parents. When they kicked me out (my parents are narcissists...decided that they didn't like being the 'heroes' after all, and said I was 'ruining their lifestyle') I had to rent. The cheapest place I could find was $400 more a month for rent than my marital home's mortgage had been - on a much smaller house with no yard. Apartments in my area are very scarce and would not be big enough for 4 kids and myself. So....I knew I had to buy.

I saved up a bit, despite being a full-time student and paying my own tuition. I got lucky and won some bursaries and scholarships so I put the money aside (I had pre-paid my tuition). As fate would have it, there was a new bunch of duplexes going up on the same street I was renting on. They were having a 'sale'. I went and looked and found it to be a kick ass deal (still expensive, but a deal for this area) as they had many energy saving initiatives that would cut my monthly utility bills, the yard would be landscaped and fenced at no extra charge, and they also had a current 'rebate' package. I was lucky enough to convince my parents to co-sign (as I am in school, not working, getting alimony and child support as my ex makes a lot of money and my parents are very well-off) and I'm now in my house. My payments are FAR more manageable than my rent was. The kids are doing so much better, we are able to paint, and hang shelves and pictures, and make this house our home. My landlord was super picky about that stuff so we were unable to personalize the rental. There was also a lack of storage space that I couldn't fix with shelving or other organizers because I was not 'allowed' to modify anything. Our landlord was always asking me to do extras for him - it was a new house, so I had to make all the appointments with the builder for fixes, he promised me a yard, then didn't deliver (we had dirt and mud for 3 years), I made all his phone calls for repairs, etc. He told me I was the best tenant ever. Then he had the nerve to increase rent!

Needless to say, this is a better option for me. The kids have a yard, I have storage space (same size house - 1500 sq ft for 5 people), I'm building up equity (accelerated weekly payments to cut down on interest) and I don't have a landlord breathing down my neck and calling me every other week to ask a favor. Overall, I'm saving hundreds every month. My utility bills are 40% less. I don't have to worry about being evicted because my landlord wants to sell the place (he mentioned he might sell a few times). I'm able to do more for my kids, we're more stable, they will go to the schools in the same town until they graduate. I'm already invested in this house. I think, where I am, it's better to let people like me buy - too many people right now are scooping up properties to rent them out, because they make a lot of money doing that. A lot of them - my landlord included- lie about it being a rental property when they buy it so they aren't putting down 25% like they are supposed to for rental properties. Those are the real 'speculators'. Those 20% rules don't stop the speculators, but they do hurt people like me who just want to pay less than rent and own their own home. I've rented and I've owned, and there really is no comparison. I hate renting, I'm not cut out for it. Renting was me throwing away my money so someone else could build up HIS equity and I got nothing out of it. At least now, I'm the one who gets the equity.

ecstatic

(32,653 posts)and got money back at closing. I'm still here (like a sucker) despite being severely underwater thanks to the foreclosure crisis. 20% equity wouldn't even begin to address how underwater I am. Money down doesn't predict whether someone can afford their home. I think one's credit report, buying/saving habits, and income is a lot more telling.

SoCalDem

(103,856 posts)and that was also when a wife's income was not included in the formula that decided if you could afford the loan.

It may seem harsh to younger people today, but it did prevent people from getting in over their heads.

Back then there were only store credit accounts (usually with very low limits) and DinersClub/AmEX (which had very high income restrictions on them)

When people got a home loan, it was assumed that they would be able to make those payments easily, and would actually pay off that house in 30 years.

There were also no equity/HELOC loans.

Foreclosures were very rare...but so were McMansions

gollygee

(22,336 posts)I would buy up a ton of income properties because there would be bunches more people needing to rent and they'll have to pay whatever it costs and compete for what rentals are available. What a great way to make rich people richer and soak people who can't afford the 20%.

Benton D Struckcheon

(2,347 posts)From a financial transaction POV, this is what you are doing:

1 - Borrowing in your country's currency, then

2 - Handing the proceeds over to buy the house and taking possession of that house.

3 - After some time (average is ten years) selling that house and getting back the currency you borrowed in step 1.

Pay attention very carefully: you are shorting your country's currency. What does that mean? That means you're betting the currency will decline relative to the cost of real estate generally, and in your area in particular.

Whenever you borrow something you are increasing its supply. Any time you increase the supply of something, you are putting downward pressure on its price. You are, in fact, shorting it, because you're betting you can pay it back later with currency units that will be worth less than they were when you borrowed it. That's the definition of a short sale in the stock market, where all you have to do is substitute shares of stock for currency units.

Ten years from now you go to sell that house, and if the currency's value has declined via inflation, you have made out (assuming no other change in real estate values affecting the area you bought in, of course). That's actually an extremely risky proposition. That inherent risk is why real estate is surrounded by huge subsidies. But if you subsidize the price of something, especially to the extent that real estate has been subsidized, you increase its price. Hence you get to the situation we have now, where it's completely unrealistic for a large segment of the population to save the standard 20% downpayment for a house.

It's a treadmill, and there's no getting off it, unless you eliminate all the subsidies, of course. But if you do that you hurt everyone who is a current homeowner.

geek tragedy

(68,868 posts)Renters are short inflation, meaning they're exposed to the risk of their gross rent rising faster than their income.

The rent is almost guaranteed to go up over time. A FRM payment doesn't.

SheilaT

(23,156 posts)I tend to think it's a good idea, but others have already posted different opinions.

When I bought my house here in Santa Fe four years ago I put 20 percent down. Got a decent interest rate and there's no mortgage insurance. I am thinking of re-financing to lower the payments and reduce the time on the loan.

I do think people need to be cautious about how much house they buy, as well as how much car they buy. In many cases it's a good idea to buy less house or less car and have less debt.

Harmony Blue

(3,978 posts)First time home buyers only require they put down 3%. I am looking to buy a home and while I am first time home buyer I am planning on putting more than 3%.

20% I can do, but most younger adults than me (under the age of 30) do not have the credit (income/debt ratio out of wack due to student loans so they don't quality for home loans) or the ability to put that much money down because they can't save when they are paying down their student loans.

In my opinion, if you are a serious home buyer you need to have at least 10% down. 20% is too high, and while 3% is the mininum threshold realistically it is easier to have a more manageable monthly mortgage if you put more than 3% down.

In Florida, it is more expensive to rent then to pay mortgage + home insurance in most areas. The housing market has bottomed out in Florida so, I am finding some nice homes for 45-55k that are 2-3 bed room/1.5 baths. In Long Island, New York similar homes likes this go for quadruple this price easily. So, it just depends where you live, but if you are a first time home buyer definitely stay away from Califorinia and New York.

But yeah the 20% threshold is not realistic given most young adults don't have that much saved up, and the sad thing is their student loan is like an albatross. They can't even qualify for a home loan because of it and that is sad what we have done to the younger generations. What is worse, is that they have started to use credit rating as a means to leverage your car insurance premiums or if you qualify to rent some upscale apartments. Generated income used to be a big factor in home loan qualitfications but credit rating has surpassed generated income in terms of importance. Not saying generated income doesn't come into play because I was told I have to be below 50% the income/debt ratio to quality for a home loan. But credit rating is more important now and most young adults simply don't have such credit due to student loans.

The pool of young adults that have the money to put down for a home and good credit is shrinking while the pool of older retiring Americans is increasing that are on fixed incomes. Something has to give at some point.